UnitedHealth Group

Section 1 — Business Overview, Operations & Competitive Positioning

1.1 The Business

sources UnitedHealth Group collects fixed monthly premiums — the majority of them ultimately funded by the U.S. government — and earns its profit on two linked spreads: the margin between premiums received and medical costs paid at UnitedHealthcare, the largest U.S. health insurer, and the fees and margins recaptured when those same health care dollars are serviced by its own care-delivery, data-analytics and pharmacy businesses under the Optum umbrella. §

The company operates through two complementary platforms. UnitedHealthcare provides health benefits across employer, individual, Medicare and Medicaid markets; Optum is an information- and technology-enabled health services business serving patients, providers, payers and life sciences organizations through three reportable segments — Optum Health (care delivery), Optum Insight (data, analytics and health-system operations) and Optum Rx (pharmacy care services). Revenue reached $447,567.0M in FY2025, up from $287,597.0M in FY2021, with growth recorded in every year of the five-year window — a scale of throughput no other company in the sector approaches. The business is overwhelmingly domestic, and its workforce is very large, with a substantial portion comprising clinical professionals — an important structural point, because UnitedHealth is as much an employer of physicians and operator of care settings as it is an insurer. The shares trade under the ticker UNH. §

How the company actually generates returns matters more than how it describes itself. The insurance businesses are working-capital engines: premiums arrive before claims are paid, generating float that is invested, while underwriting margin depends on pricing medical cost trend accurately twelve months in advance. The Optum businesses then re-intermediate the same dollar — a premium collected by UnitedHealthcare can be spent at an Optum-owned clinic, processed on an Optum Insight platform and filled through an Optum Rx pharmacy — so the consolidated return on a member is the sum of an underwriting spread and several service margins. FY2025 was a transition year for this model: management concedes in the filing that its pricing and health-status assumptions fell well short of the medical cost trend actually incurred, significantly impacting earnings, and the year closed with a broad restructuring program under a substantially new leadership team. Those dynamics are examined in Sections 2 and 3; the model itself, described here, remains intact.

Key Information

| Item | Value |

|---|---|

| Ticker | UNH |

| Sector / Industry | Healthcare — Managed Care |

| Report Date | 2026-06-07 |

| Most Recent FY Revenue | $447,567.0M |

| EBIT Margin (Most Recent FY) | 4.2% |

| Diluted Shares Outstanding | 911M |

| Current Price | $399.47 |

| Rating | HOLD |

| 12-Month Price Target | $364.86 |

| Conviction | Medium |

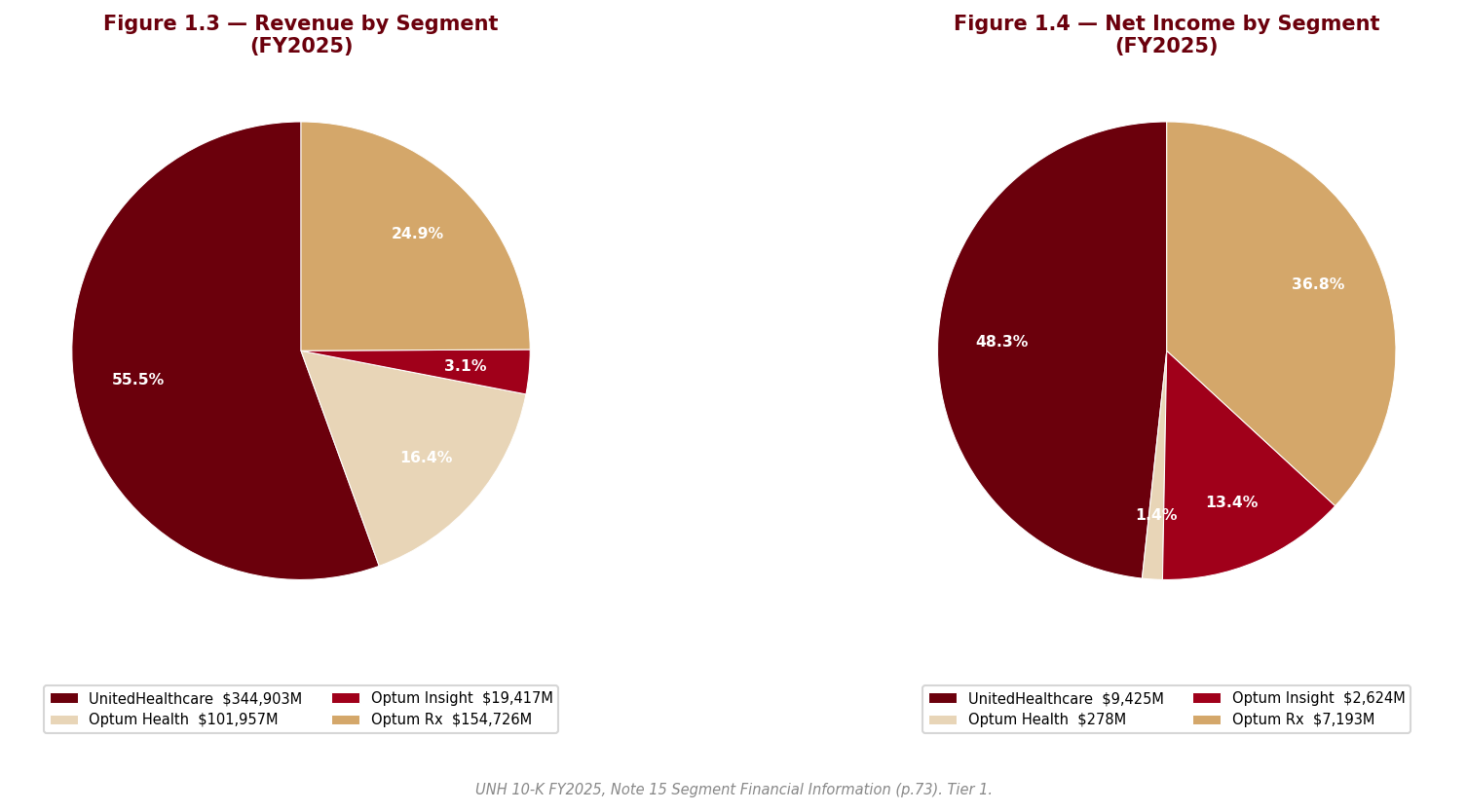

1.2 Operating Segments

sources UnitedHealthcare is the benefits franchise, organized across three businesses. Employer & Individual sells risk-based plans — in which the company assumes medical and administrative cost responsibility in exchange for a fixed monthly premium — alongside fee-based administrative services for self-funded employers who retain the risk themselves. Medicare & Retirement serves seniors through Medicare Advantage, where CMS pays a fixed monthly premium per member that varies with geography, demographics and the member’s coded health status, plus Part D drug coverage and Medicare Supplement products; premium revenues from CMS represent a very substantial share of total consolidated revenues, making the federal government the company’s most important counterparty by a wide margin. Community & State manages Medicaid and related safety-net programs under per-member monthly premiums from state governments, won through formal bid processes. The single economic variable that drives the entire segment is the medical care ratio — the share of each premium dollar consumed by claims. Premiums are fixed for the contract period, so cost trend that exceeds the priced assumption cannot be recovered until the next pricing cycle; small forecasting errors translate into large earnings swings.

Optum Health is the care-delivery arm: primary, specialty and surgical care across clinic, in-home and virtual settings, with an explicit strategy of moving providers from fee-for-service to value-based arrangements. In its fully accountable value-based contracts, Optum Health takes responsibility for a patient’s total cost of care in exchange for a monthly premium — economically, it becomes a mini-insurer with delivery assets. The driving variable is therefore the same as UnitedHealthcare’s, transposed: medical cost per capitated member versus the premium received. This symmetry is the segment’s strength in benign cost environments and its central fragility when trend runs hot, as FY2025 demonstrated. The segment historically also housed Optum Financial, including Optum Bank, which earns fees plus investment and interest income on consumer health accounts; effective at the start of the new fiscal year, Optum Financial moves to Optum Insight, with prior periods to be recast — a comparability break analysts should anticipate in quarterly reporting.

Optum Insight sells services, analytics and software platforms that run clinical, administrative and financial processes for health systems (revenue cycle management), health plans (payment integrity, risk and quality), state governments (Medicaid program administration) and life sciences companies. Products are typically delivered over multi-year contracts, and the segment maintains an order backlog of signed agreements and anticipated renewals — making backlog conversion the variable to watch. A portion of that backlog relates to affiliated agreements with other UnitedHealth businesses, a point developed below.

Optum Rx is the pharmacy care platform: a pharmacy benefit manager combined with home-delivery, specialty, community and infusion pharmacies, including limited-distribution oncology and gene-therapy support capabilities. Its economics are driven by script volume and the retained spread on managed drug spend — a scale business in which purchasing leverage compounds with size.

The system view. The four segments form a deliberate flywheel: UnitedHealthcare’s membership supplies patients to Optum Health’s clinics, claims to Optum Insight’s platforms and scripts to Optum Rx; Optum’s cost-management and care-steering capabilities in turn protect UnitedHealthcare’s underwriting margin; and the data generated at every node feeds back into pricing, risk coding and clinical engagement. Management frames the acceleration of value-based care as the core growth strategy precisely because it deepens every one of those linkages. The fragilities are the mirror image. First, the intersegment revenues eliminated in consolidation are priced at management’s estimate of fair value — meaning reported segment margins are partly an internal allocation choice rather than a market outcome, and a growing share of Optum Insight’s backlog is affiliated rather than won from third parties, so its growth is increasingly captive rather than market-validated. Second, the flywheel correlates exposures rather than diversifying them: when Medicare Advantage funding compresses, UnitedHealthcare’s premiums and Optum Health’s capitation revenues are hit by the same policy decision simultaneously, which is exactly the pattern that produced the FY2025 result. Third, the integrated model concentrates regulatory and political attention on a single corporate entity. The flywheel is real, but FY2025 showed that it spins in both directions.

1.3 Geographic Exposure

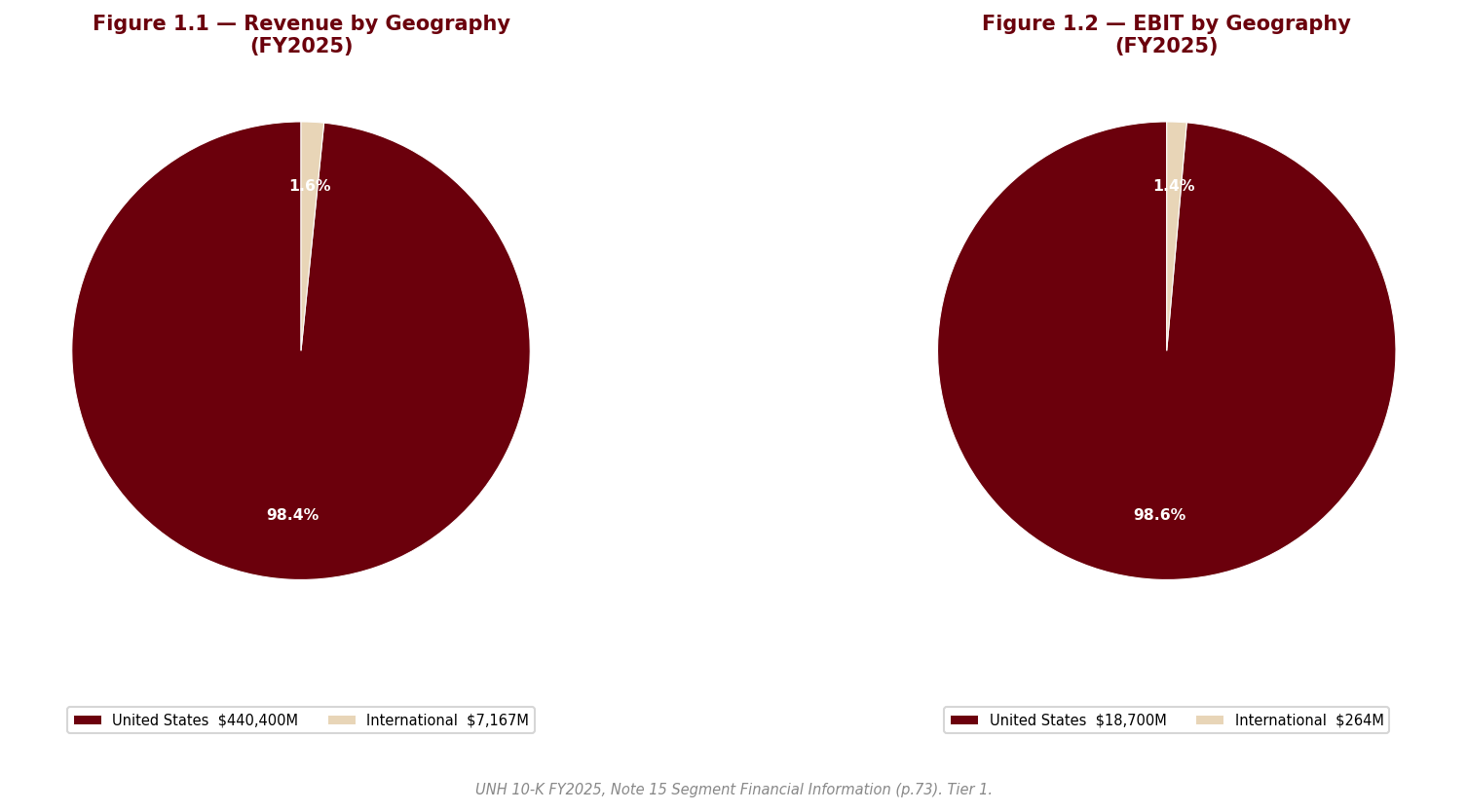

sources UnitedHealth Group is, for analytical purposes, a domestic U.S. business. Its members, providers, payers and regulators are overwhelmingly American, and currency exposure is immaterial to the investment case. The residual international footprint is being reduced rather than grown: the year’s portfolio review included business exits and dispositions, and the remaining South American operations are held for sale. The meaningful concentration is therefore not geographic but payer-based — a very substantial share of consolidated revenue flows from a single counterparty, CMS, supplemented by state Medicaid agencies. That concentration, and the rate-setting and investigative powers that come with it, is the dominant exposure of the company and is treated in depth in Section 2.

1.4 Management Team

sources The leadership team was almost entirely rebuilt within roughly twelve months — an extraordinary reset for a company of this size, and itself a fact the analysis must price. Stephen Hemsley, the long-tenured former chief executive, returned as Chair and Chief Executive Officer in May 2025, combining the two roles and reversing the prior separation. Wayne DeVeydt joined as Chief Financial Officer in September 2025 from Bain Capital, having previously run Surgery Partners and served as finance chief of Elevance Health — the closest peer — which makes him one of the few external hires who arrives already fluent in managed-care economics. Dr. Patrick Conway took over as CEO of Optum in May 2025, and Tim Noel became CEO of UnitedHealthcare in January 2025. §

The anchor is unambiguously Hemsley: his return is a credibility transaction with the market, trading continuity and operational memory for a renewed — and now larger — succession question, since a returning former CEO is by construction a bridge rather than a destination. DeVeydt’s appointment is the most substantive signal; an outside CFO from the principal competitor suggests the Board wanted an unsentimental view of the portfolio, and the broad restructuring program that arrived in the new team’s first full quarter is consistent with that mandate. The risks are equally clear and are flagged as a watch item: the majority of listed executive officers are new or newly in role, execution depends on a team that has not yet operated together through a full pricing cycle, and the bench beneath them is unproven at this scale. The governance dimensions of the transition, including the circumstances of the UnitedHealthcare CEO succession, are addressed in Section 2.

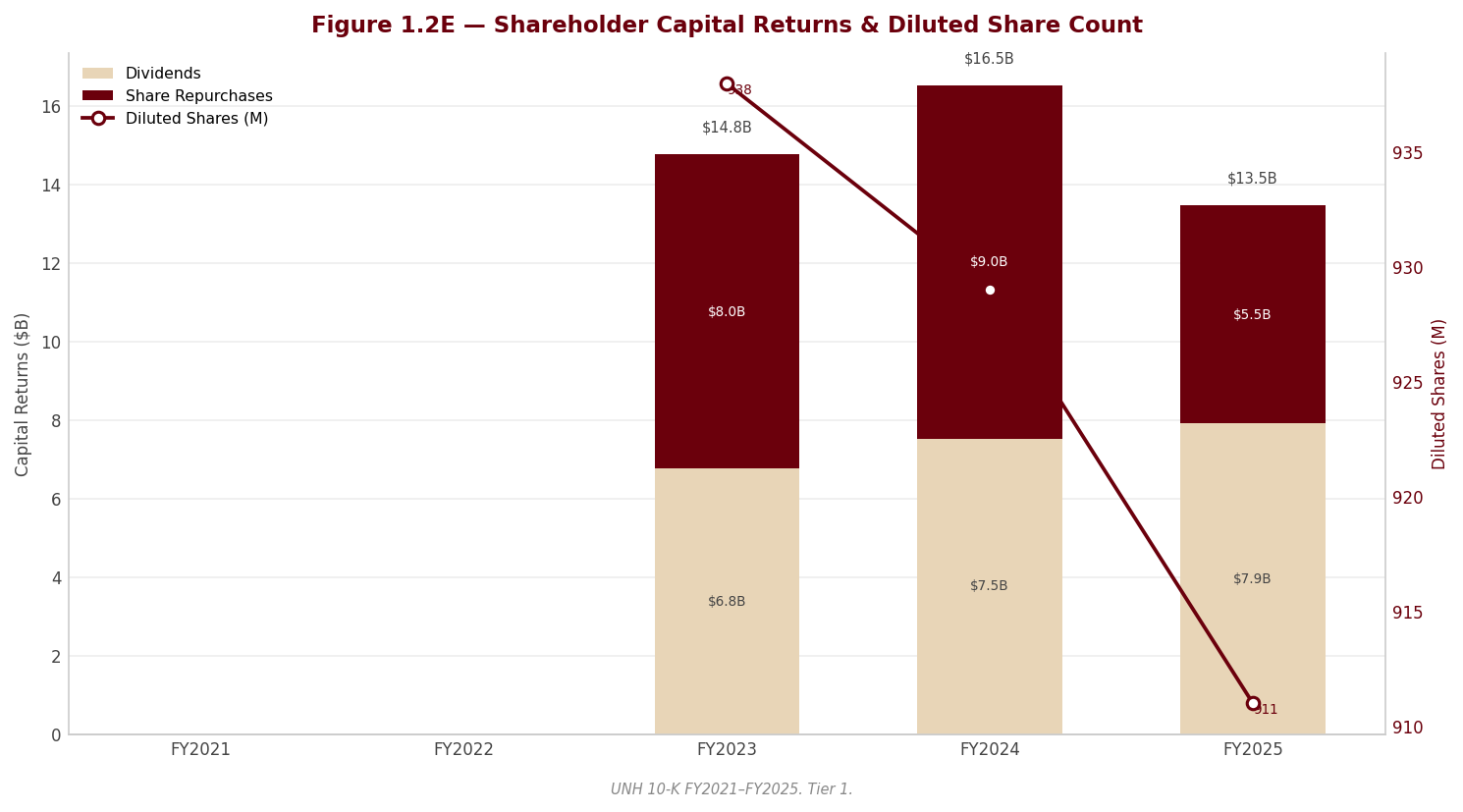

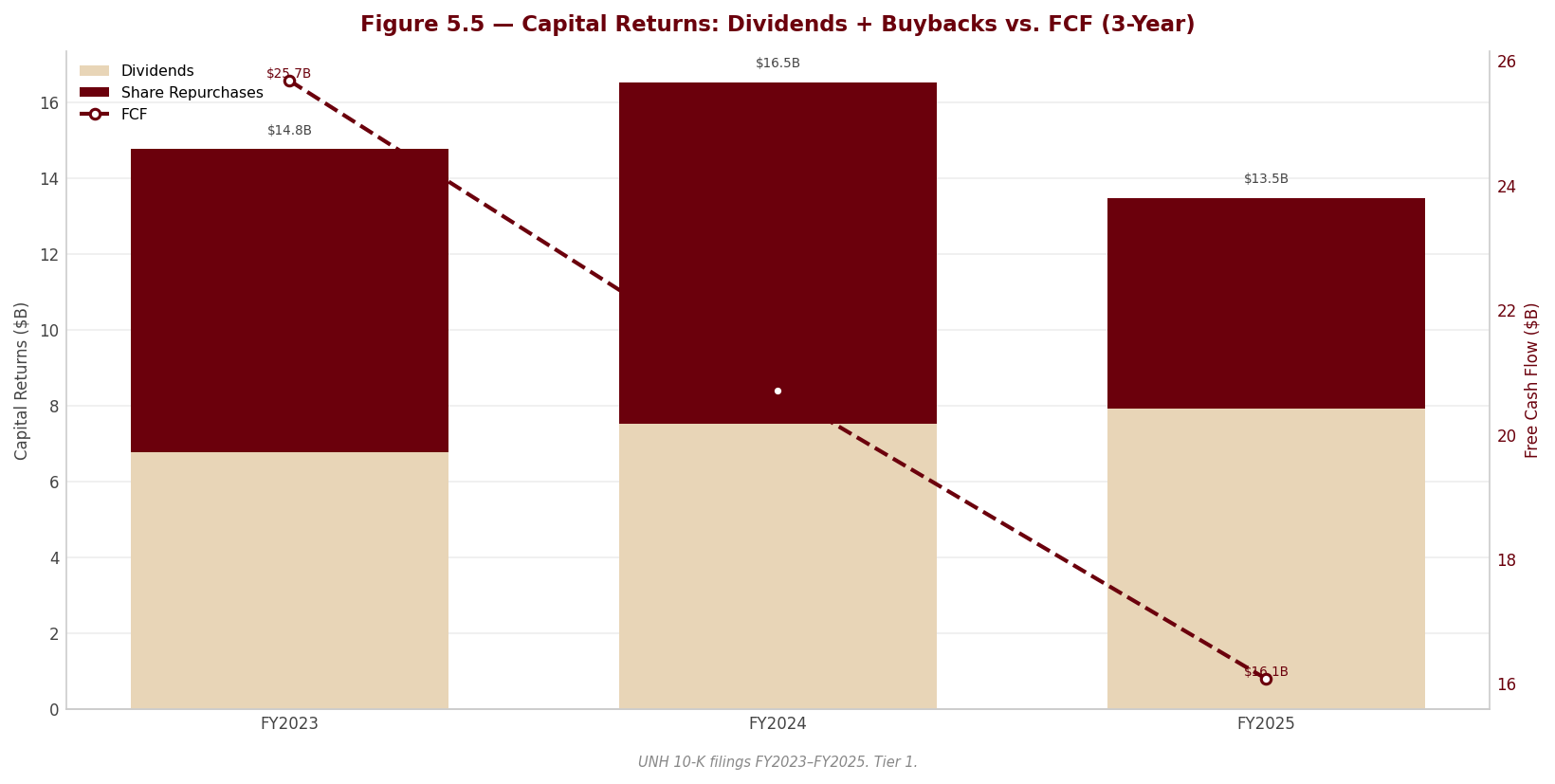

1.5 Capital Allocation Track Record

sources | Year | Dividends Paid ($M) | Share Repurchases ($M) | CapEx ($M) | |—|—|—|—| | FY2021 | $-5,280.0M | $-5,000.0M | $-2,454.0M | | FY2022 | $-5,991.0M | $-7,000.0M | $-2,802.0M | | FY2023 | $-6,761.0M | $-8,000.0M | $-3,386.0M | | FY2024 | $-7,533.0M | $-9,000.0M | $-3,499.0M | | FY2025 | $-7,916.0M | $-5,545.0M | $-3,622.0M |

Source: UNH 10-K FY2025, Consolidated Statements of Cash Flows; Data sheet, UNH_Portfolio.xlsx.

The structural pattern of the past five years is that of a capital-light services compounder: capital expenditure is modest relative to the revenue base because the company’s growth has historically been bought, not built — acquisitions of physician practices, technology platforms and pharmacy assets are the true reinvestment channel, which is why goodwill and intangibles dominate the balance sheet (a risk treated in Section 2). What the business did not spend on plant, it returned: a quarterly dividend raised consistently, paired with sustained share repurchases.

FY2025 marks an inflection in that pattern that deserves more attention than the table alone conveys. The Board raised the quarterly dividend mid-year even as earnings came under severe pressure — signaling that the dividend is treated as a quasi-fixed commitment — yet no share repurchases occurred in the closing months of the year. The buyback, in other words, is the swing variable, and it swung to zero at the same time that the regulated insurance subsidiaries required net capital infusions from the parent rather than paying dividends up to it, a reversal of the system’s normal cash direction. Repurchases executed earlier in the year were made at average prices well above where the stock ended it, an unflattering timing record. Taken together, the FY2025 actions read as a shift from shareholder-return maximization to balance-sheet protection within a single year; the liquidity mechanics behind that shift, including rising statutory capital requirements, are analyzed in Sections 2 and 3. Investors should not assume buyback support for the share count in the coming year until subsidiary dividend capacity normalizes.

1.6 Competitive Positioning & Moat

sources §1.6.1 Industry structure. U.S. health care spending has grown consistently for many years, accounts for a substantial share of GDP, and is expected by management to keep growing on demographics, medical technology and pharmaceutical advancement. The structure of managed care concentrates returns in scale: a larger insurer spreads fixed administrative and technology cost over more members, negotiates deeper provider discounts, and absorbs actuarial volatility that would impair a subscale book. Critically, the growth payer is the government — Medicare Advantage and Medicaid — which means the entity that sets prices is also the largest customer. Returns therefore accrue to operators who can manage realized medical cost trend below the trend embedded in fixed premiums, year after year, across a rate cycle they do not control.

§1.6.2 Competitive advantages. UnitedHealth’s moat rests on four pillars, each anchored in the filing rather than asserted. First, absolute scale: a $447,567.0M revenue base — the largest in the industry — directly funds the network discounts, technology investment and actuarial depth that the industry structure rewards. Second, vertical integration: no competitor pairs the largest benefits franchise with owned care delivery, a health-system-wide analytics business and a top-tier pharmacy benefit manager; management’s stated strategy of accelerating fully accountable value-based care is, in moat terms, a mechanism for converting insurance scale into recurring service revenue that fee-only rivals cannot replicate. Third, local network depth: the company itself frames its UnitedHealthcare positioning around strong local-market provider relationships, breadth of product, and competitive medical and operating cost positions — advantages that are accumulated market by market and are slow for entrants to assemble. Fourth, contracted visibility: Optum Insight’s multi-year order backlog of signed and legally binding agreements gives a portion of the services business revenue character closer to software than to insurance. It is worth noting that management describes its own markets as highly competitive, with rivals ranging from startups to sophisticated global enterprises; the moat is scale and integration, not the absence of competition.

§1.6.3 Competitive vulnerabilities. The vulnerabilities are concentrated where the moat is deepest. The same government concentration that funds growth exposes the company to a payer that has been setting Medicare Advantage rates below forward medical cost trend for multiple years, with risk-model revisions reducing funding further — a pressure management itself describes as sustained and which no degree of scale offsets, because it applies to the whole industry’s largest channel at once. Underwriting is repricing-lagged: FY2025 proved that when management misjudges trend, the fixed-premium model transmits the error directly to earnings, and the company has now under-forecast trend through consecutive cycles. The integrated model invites regulatory and antitrust scrutiny precisely because of its breadth, and the pharmacy benefit management business faces an active legislative and investigative agenda industry-wide. Unresolved federal investigations touching Medicare billing practices — disclosed in the filing only in general terms — sit directly on the largest revenue source, and are treated as the dominant regulatory risk in Section 2. Finally, the partly self-referential nature of segment economics (internally priced intersegment revenue, a growing affiliated share of Optum Insight’s backlog) means the market-validated portion of Optum’s growth is smaller than headline segment figures suggest.

§1.6.4 Verdict. The competitive position is genuinely strong and was not the cause of the FY2025 setback: no rival took UnitedHealth’s members, networks or pharmacy scale. What FY2025 demonstrated is that the moat protects market position, not margins, when the dominant payer cuts effective rates and the company misprices medical cost trend simultaneously. The structural advantages — scale, integration, data, distribution — should allow the company to defend share and to reprice faster than subscale peers, which argues for margin recovery being a question of timing rather than possibility. But the through-cycle margin in the government businesses is likely to settle structurally below the levels of the past decade, with the Optum recapture model the principal offset. Long-run margin durability therefore rests less on competition than on two things outside the moat’s reach: the Medicare rate cycle, and management’s restored underwriting discipline. Both are testable within the next two pricing cycles, and Section 3 frames the evidence.

Section 2 — Key Risks & Catalysts

2.1 Downside Risks

sources The risk landscape at UnitedHealth Group is dominated by a single counterparty — the federal government — which simultaneously sets the prices for the company’s largest revenue source, audits the coding that determines those prices, and is now investigating the company’s billing practices; layered beneath that regulatory nucleus, the forensic review of the FY2025 filing surfaced an unusual concentration of red-flag findings in earnings quality, reserve adequacy, holding-company liquidity and balance-sheet composition, several of which are new to this filing year. This is not a normal risk profile for an investment-grade compounder, and the section that follows treats it accordingly: the risks below are specific findings from this filing, not sector boilerplate, and in our judgment they currently outweigh the identifiable catalysts.

Risk 1 — Federal Medicare-billing investigations: unnamed, unreserved and unbounded

sources This is the dominant risk in the filing, and it is flagged at the highest severity by our forensic review — as much for how it is disclosed as for what it is. The Department of Justice’s criminal and civil investigations into the company’s Medicare billing practices, which the company itself publicly confirmed in mid-2025, are nowhere specifically named in the 10-K. The commitments and contingencies footnote covers them only with generic language: a list of government agencies that review the company’s businesses, and a single sentence acknowledging that certain businesses have been or are under review for compliance with coding and other requirements under the Medicare risk-adjustment model. No liability is accrued. No range of loss is provided. The company states it is often unable to estimate losses or ranges of losses for such matters — which means that any settlement, civil penalty, corporate integrity agreement or, at the extreme, program exclusion would be entirely incremental to reported results, with no reserve standing in front of it. The only named DOJ matter remains the long-running False Claims Act whistleblower case dating to 2011.

The exposure sits directly on the company’s largest revenue source. Premiums from CMS are the single biggest component of consolidated revenue and grew as a share of the total this year, so the entity conducting the investigation is also the company’s most important customer. The mechanics of Medicare Advantage compensation — fixed monthly premiums that vary with each member’s coded health status — place risk-adjustment coding at the center of both the revenue model and the investigation, and the filing separately confirms that some of the company’s local plans have been selected for risk-adjustment data validation audits, which can produce retrospective payment adjustments.

Two adjacent findings sharpen the picture. First, the forensic comparison against the prior-year filing found that the word “shareholders” was quietly added to the list of parties bringing legal actions against the company — new language this year, and an oblique acknowledgment of securities litigation following the 2025 share-price collapse, with no further detail given. Second, as a partially offsetting watch item, the 2011 False Claims Act case took a procedurally favorable turn: a court-appointed Special Master recommended summary judgment in the company’s favor on all remaining claims, though the DOJ has moved to reject that recommendation and the matter remains open. The court’s eventual ruling will be read as precedent for the broader risk-adjustment exposure, in both directions.

Probability: High (that the investigations remain a live, unpriced overhang through the forecast horizon) | Timeframe: Immediate | Quantified potential impact: Not quantifiable by design — the company provides no accrual and no range, which is itself the finding. The relevant frame is that outcomes span a wide distribution from dismissal to a settlement with conduct remedies, and any adverse resolution would fall entirely outside reported reserves while potentially constraining the risk-coding practices that support Medicare Advantage revenue itself.

Risk 2 — The reserve cushion is gone: underwriting risk with no buffer

sources UnitedHealth’s risk-based products collect fixed premiums and pay uncertain claims, so reported earnings rest on two actuarial estimates: the pricing assumption set a year in advance, and the reserve for claims incurred but not yet reported. The FY2025 filing shows both legs under strain simultaneously. Management concedes in the MD&A that its pricing and health-status assumptions fell well short of incurred medical cost trend, significantly impacting earnings — an unusually candid admission, and the second consecutive cycle in which trend was under-forecast. More structurally, our forensic review flags at the highest severity that the favorable prior-year reserve development which historically released into earnings each year has declined sharply for the third consecutive year and is now a small fraction of its level two years ago. The cushion of conservatism is essentially exhausted: the reported medical care ratio is now a “truer” — and structurally higher — number than in prior years, and there is far less buffer if claims trend deteriorates from here.

The same footnote contains a first-time disclosure that confirms the direction of travel: a premium-deficiency and loss-contract reserve line appears in the medical-costs-payable rollforward for the first time, an explicit acknowledgment that certain books of business are priced below expected cost. The estimation machinery itself remains the auditor’s sole critical audit matter — the IBNR estimate for medical costs payable — and the filing’s own sensitivity disclosure makes clear that small changes in completion factors or per-member cost trend move the reserve by amounts material to net earnings. The risk-factor disclosure says the rest plainly: relatively small differences between predicted and actual medical costs have resulted, and may again result, in significant changes in financial results, and cost overruns cannot be recovered within the fixed premium period.

Probability: Medium | Timeframe: Immediate to 1–2 years | Impact: A renewed underwriting miss in 2026 would flow directly to earnings with no development buffer to absorb it, would push the medical care ratio — and therefore required statutory capital — higher still, and would compound Risks 4 and 5 below. The filing’s own sensitivity framing establishes that the swing from modest estimation error alone is material to net earnings.

Risk 3 — A kitchen-sink transition year: the 2026 “recovery” may be partly manufactured

sources Two of the forensic review’s highest-severity findings concern the quality of the FY2025 baseline itself, and they matter prospectively because every recovery narrative will be measured against it. First, the fourth-quarter “restructuring and other actions” charge is a bundle that sweeps in items which are not restructuring in any conventional sense: net valuation losses on equity securities (an investment result), the advance funding of the company’s charitable foundation (a discretionary contribution), and — most importantly — the establishment of a loss-contract reserve that pulls anticipated 2026 losses at certain Optum Health value-based care businesses into 2025. Management itself states that the net cash-flow impact of these actions in the coming year is expected to be immaterial, confirming that the charges are largely non-cash or accrual-timing in nature. The pattern is a classic big-bath: depress the transition year, pre-book the next year’s losses, and create an easier comparison base. As the loss-contract reserve is released against actual 2026 costs, reported segment results will be flattered by exactly the amount that was pulled forward.

Second, and cutting in the opposite direction within the same year, the company recorded a large non-cash gain on the deconsolidation of a business — triggered not by a sale but by “changes in governance rights” — and booked that gain inside operating costs, where it is the principal driver of the net portfolio gain attributed to Optum Rx and therefore of that segment’s reported earnings growth. No cash was received; the retained stake is now an equity-method investment measured at the least observable level of the fair-value hierarchy, and the identity of the deconsolidated business is not disclosed. A governance-rights change that produces a gain of this character inside a reportable segment’s operating result deserves more disclosure than it received.

The context is unavoidable: these actions land in the first full quarter of an almost entirely new leadership team — returning CEO, externally hired CFO, new chief executives at both Optum and UnitedHealthcare, all within roughly twelve months — which is noted as a governance watch item in its own right. The timing of the charges is consistent with a new team resetting the base from which it will be measured. The filing also makes no reference of any kind to the December 2024 killing of the UnitedHealthcare chief executive that preceded this succession; we note the omission without speculating beyond filed facts. The practical consequence for investors: neither FY2025 segment results (especially Optum Health’s operating loss) nor any apparent FY2026 margin recovery should be taken at face value — both must be read net of the reserve pull-forward, the non-recurring charges and the deconsolidation gain.

Probability: High (that reported 2026 improvement overstates underlying improvement) | Timeframe: 1–2 years | Impact: This is a risk to analytical conclusions and to the durability of any re-rating rather than to cash flows directly: if the market capitalizes a manufactured margin recovery, the disappointment arrives when the reserve releases and easy comparisons lapse. Section 3 decomposes the affected figures.

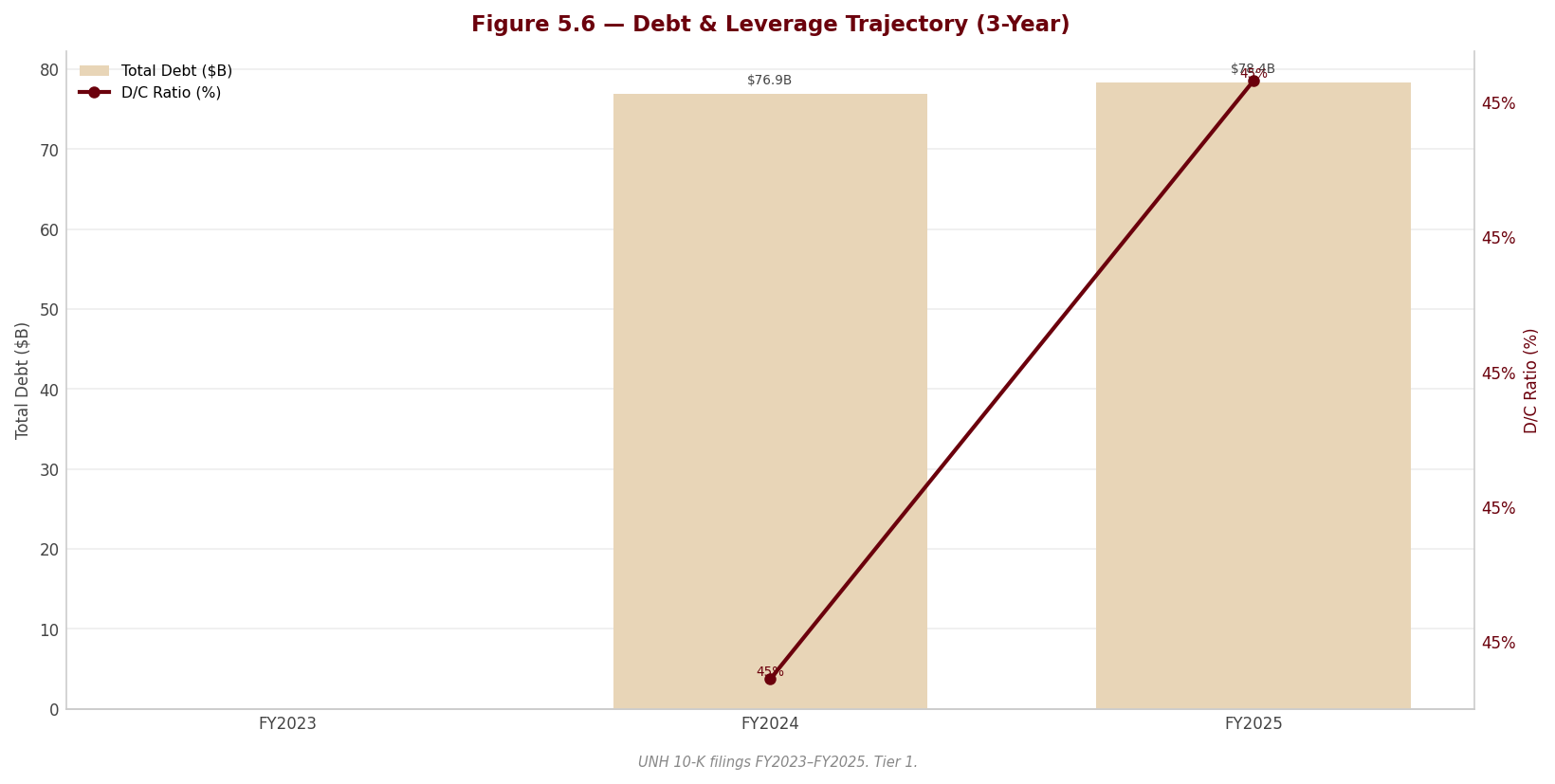

Risk 4 — Holding-company liquidity has reversed: subsidiaries now absorb capital

sources A cluster of mutually reinforcing disclosures, flagged at the highest severity, shows the group’s internal cash engine running backwards. In FY2025 the regulated insurance subsidiaries received net capital infusions from the parent — a reversal from the prior year, when they paid very large net dividends up to it — while only a small fraction of consolidated cash and equivalents is available for general corporate use. The parent-company-only schedule shows the holding company increasingly funded by intercompany notes from its own subsidiaries: it is borrowing from the entities it owns to service external debt, the dividend and buybacks. And because the elevated medical care ratio raises the statutory capital its insurance subsidiaries must hold, the company has entered reinsurance agreements explicitly to reduce capital and surplus requirements — agreements that do not qualify for reinsurance accounting and are carried under deposit accounting, meaning no risk transfer is recognized. That is capital engineering, not risk transfer, and it signals genuine pressure on regulated-entity surplus. §

A second highest-severity finding compounds the picture on the cash-flow statement: the company entered a new, short-dated (under one year), uncommitted receivables-sale facility in 2025 — no such facility existed in the prior-year filing — under which receivables sold to banks are recorded as a reduction of receivables and classified as operating cash flow. Management’s own MD&A lists the sale of receivables among the supports to operating cash flow in a year when operating cash flow declined. Because the facility is uncommitted and matures within a year, the benefit reverses if the banks decline to renew, converting a financing-like dependence into an operating-cash-flow headwind. Reported FY2025 cash conversion is therefore flattered, and Section 3 footnotes the affected metrics.

The surrounding signals are consistent with strain: share repurchases stopped entirely in the closing quarter; the major rating agencies hold predominantly negative outlooks on the senior debt; and the commitments footnote discloses, for the first time as a quantified commitment, put and call options on unconsolidated businesses created by the portfolio-refinement program — a contingent, largely counterparty-controlled claim on parent liquidity that sits outside the balance sheet (a watch item in its own right). Against this, the debt structure itself is clean — committed revolvers undrawn, maturities laddered, covenant compliance asserted — so this is a risk of capital-flow direction and flexibility, not of near-term solvency.

Probability: Medium | Timeframe: Immediate to 1–2 years | Impact: Dividend capacity, buyback resumption and deleveraging all depend on the medical care ratio normalizing so that subsidiaries can resume up-streaming cash. If 2026 medical costs disappoint again, the negative rating outlooks become live downgrades, raising funding costs precisely when the parent’s internal funding sources are already strained — and the put/call obligations could be exercised into that weakness.

Risk 5 — Goodwill concentration against a loss-making segment

sources Goodwill and other intangibles represent a dominant share of total consolidated assets — a balance-sheet composition the company’s own risk factors flag as exposed to material impairment if acquired businesses underperform the assumptions used to value them. The forensic review pairs that concentration with an uncomfortable fact pattern flagged at the highest severity: Optum Health, the reporting unit carrying the largest goodwill balance of the four, swung to an operating loss in FY2025, required a loss-contract reserve for anticipated further losses in its value-based care book in 2026, and is guided to serve fewer value-based care lives — yet its goodwill increased during the year through continued acquisitions. Management asserts that the annual impairment test found all reporting units’ fair values “substantially in excess” of carrying values, but discloses no quantitative headroom, discount rates or growth assumptions, making the assertion untestable as disclosed. Meanwhile, the businesses the company is actually selling tell a less comfortable story: held-for-sale remeasurements crystallized losses, meaning exit values came in below carrying values for the assets being divested.

The trigger to watch is the 2026 repricing of the value-based care book. If the economics do not recover on repricing — and management has already pre-booked losses for part of that book — impairment risk migrates from theoretical to live. A charge would be non-cash, but it would directly reduce the equity base supporting credit ratings already on negative outlook, and it would constitute an admission that a meaningful portion of the acquisition-led growth strategy was overpaid for. §

Probability: Medium | Timeframe: 1–2 years | Impact: Non-cash but ratings-relevant and narrative-defining: an Optum Health impairment would simultaneously weaken the credit-metric equity base (compounding Risk 4) and undercut the central pillar of the long-term thesis — that value-based care delivery converts insurance scale into durable service margins.

Additional watch items. Three lower-severity forensic findings warrant monitoring without rising to standalone risks. The Change Healthcare cyberattack of early 2024 remains a live earnings drag: the company took a further fourth-quarter reserve against collections on the interest-free loans it extended to affected providers, receivable allowances rose, and the litigation and regulatory tail from the data breach is not quantified anywhere in the contingencies footnote — even as the cybersecurity item asserts no material threats were identified as of year-end. Second, intersegment economics deserve skepticism: internal transactions are priced at management’s estimate of fair value, affiliated revenues eliminated in consolidation grew faster than consolidated revenue, a growing share of Optum Insight’s backlog is affiliated rather than market-won, and the 2026 segment realignment (Optum Financial moving from loss-making Optum Health into margin-compressing Optum Insight, with prior periods recast) must be checked for whether the recast obscures deterioration in either segment. Third, Optum Bank’s loan book is growing rapidly, with consumer lending expanding fastest, commercial mortgages collateralized by commercial real estate, a meaningful portion of loans carried at fair value using unobservable inputs, and funding drawn primarily from HSA deposits — adding a credit and asset-liability dimension that is not core to the health-services thesis.

2.2 Upside Catalysts

sources The catalyst picture is thinner than the risk picture, and we state that plainly: this is a five-risk, three-catalyst profile, and the catalysts are predominantly recovery mechanics — the unwinding of 2025’s damage — rather than new sources of value creation. None is a pure binary windfall; each requires execution against a medical cost trend that management itself expects to persist and has mis-forecast for two consecutive cycles.

Catalyst 1 — The 2026 repricing and benefit redesign restore underwriting margin

sources The most consequential catalyst is the simplest: the fixed-premium model that transmitted the 2025 underwriting miss directly to earnings works symmetrically on the way back. Management has repriced and redesigned benefits for 2026 with the elevated care patterns explicitly contemplated, is deliberately shrinking to restore margin — Medicare Advantage membership, Medicaid membership (including exit from one state) and value-based care lives are all guided to contract — and retains the levers the MD&A enumerates: network composition, benefit adjustments, supplemental premiums and county-by-county participation decisions. The final rate notice for 2026 approached the industry’s forward cost trend, a better starting point than the prior multi-year shortfalls. If realized trend lands within the new pricing corridor, the medical care ratio falls, statutory capital pressure eases, and the recovery becomes self-funding through Risk 4’s machinery in reverse — subsidiary dividends resume, and the holding-company strain unwinds. The essential caveat comes from Risk 3: part of the apparent 2026 improvement is pre-arranged through the loss-contract reserve, so the genuine signal is the medical care ratio excluding reserve releases, not headline segment margin. §

Probability: Medium | Timeframe: 1–2 years | Monitoring trigger: Quarterly medical care ratio against priced trend through 2026, read alongside the rollforward of the loss-contract reserve — improvement driven by reserve releases is noise; improvement in the underlying ratio is signal. Membership attrition running materially beyond guidance would indicate the repricing is overshooting.

Catalyst 2 — Favorable resolution of the 2011 False Claims Act case

sources The court-appointed Special Master has recommended summary judgment in the company’s favor on all remaining claims in the long-running risk-adjustment whistleblower case — the most procedurally favorable posture this matter has reached. The DOJ has moved to reject the recommendation, so the outcome is genuinely open, but adoption of the report by the court would do more than close one case: it would set a read-through precedent on the legal theory underlying risk-adjustment coding liability, the same terrain on which the broader unnamed investigations (Risk 1) operate, and would likely compress the legal-overhang discount embedded in the equity. This is the closest thing in the filing to a binary upside event. §

Probability: Medium | Timeframe: 1–2 years (court timing is not in the company’s control) | Monitoring trigger: The court’s ruling on the Special Master’s report and the DOJ’s objection; any subsequent appellate posture. Symmetrically, rejection of the report would harden Risk 1.

Catalyst 3 — Normalization of subsidiary dividends and resumption of capital returns

sources The same disclosures that constitute Risk 4 define the recovery signature. If the medical care ratio improves, the sequence runs: required statutory capital stabilizes, the deposit-accounted reinsurance scaffolding becomes unnecessary, regulated subsidiaries resume paying dividends to the parent rather than absorbing infusions, the receivables facility can lapse without straining cash flow, rating outlooks revert to stable, and the suspended buyback — historically the company’s principal return channel, with authorization still outstanding — resumes against a depressed share price. Each step is observable in filings, which makes this catalyst unusually monitorable. The dividend increase pushed through mid-2025 despite the earnings collapse signals the Board treats the dividend as a fixed commitment; the buyback is the swing variable and its restart would be the market’s confirmation that management itself believes the balance-sheet pressure has passed.

Probability: Medium | Timeframe: 1–2 years | Monitoring trigger: Direction of parent/subsidiary capital flows and intercompany note balances in the next annual filing’s parent-only schedule; renewal or lapse of the receivables facility at its maturity; rating-outlook revisions; first quarter with resumed repurchases.

2.3 Risk & Catalyst Summary

sources | # | Item | Type | Probability | Timeframe | Status | Monitoring Trigger | |—|—|—|—|—|—|—| | 1 | Federal Medicare-billing investigations — unnamed, unreserved, unbounded | Risk | H | Immediate | Active | First named disclosure, accrual or settlement framework in any 2026 filing; RADV audit outcomes | | 2 | Reserve cushion exhausted — underwriting risk with no buffer | Risk | M | Immediate–2 years | Active | Prior-year development line and premium-deficiency reserve in next medical-costs-payable rollforward | | 3 | Kitchen-sink baseline — 2026 recovery partly manufactured | Risk | H | 1–2 years | Active | Loss-contract reserve releases vs actual 2026 Optum Health results; quality of segment recast | | 4 | Holding-company liquidity reversal and cash-flow propping | Risk | M | Immediate–2 years | Active | Parent/subsidiary capital-flow direction; receivables-facility renewal; rating-outlook actions | | 5 | Goodwill concentration against loss-making Optum Health | Risk | M | 1–2 years | Latent | VBC repricing outcome in 2026; any quantitative headroom disclosure or triggering-event test | | 6 | 2026 repricing and benefit redesign restore underwriting margin | Catalyst | M | 1–2 years | Monitoring | Underlying MCR ex-reserve-releases vs priced trend; membership attrition vs guidance | | 7 | Favorable resolution of the 2011 False Claims Act case | Catalyst | M | 1–2 years | Monitoring | Court ruling on Special Master report and DOJ objection | | 8 | Subsidiary dividend normalization and capital-return resumption | Catalyst | M | 1–2 years | Monitoring | Parent-only schedule capital flows; buyback restart; outlook revisions to stable |

2.4 Risk Interdependencies

sources These risks do not sit side by side; they share a single transmission mechanism, and that is what makes the profile more dangerous than the sum of its parts. The nucleus is CMS: one counterparty simultaneously supplies the largest share of revenue, sets the rates that have run below cost trend for multiple years, administers the risk-adjustment model whose revision is cutting funding, audits the coding that determines payment, and houses the enforcement arm investigating that same coding. A hostile turn on any one of those faces tightens all the others. The financial risks then chain off that nucleus in a defined sequence: if 2026 medical costs disappoint again (Risk 2), the medical care ratio stays elevated, which mechanically raises required statutory capital, which deepens the subsidiary capital absorption and parent funding strain (Risk 4), which converts negative rating outlooks into downgrades just as the uncommitted receivables facility and the put/call obligations can call on liquidity. A failed value-based care repricing — the same event, viewed from the asset side — is also the trigger for an Optum Health goodwill impairment (Risk 5), which would strike the equity base supporting those ratings in the same period. Risk 3 then degrades the instrumentation: because the 2025 baseline was depressed by pulled-forward losses and flattered by a non-cash gain, the early-warning value of reported 2026 margins is impaired — reserve releases can make a deteriorating book look like a recovering one for several quarters, delaying recognition of exactly the scenario described above. The single most damaging combination is a second underwriting miss coinciding with an adverse development in the DOJ matters: the first removes the financial flexibility, the second arrives as an unreserved claim against it, and the disclosure posture of the filing means neither is currently priced into reported figures. Conversely, the dependencies work in reverse — a clean underwriting year releases the entire chain at once, which is why Catalyst 1 dominates the upside case.

2.5 ESG & Regulatory Exposure

sources The regulatory exposure in this filing is unusually concrete and sits well above generic sector risk. On Medicare Advantage, management states that rate notices for numerous years have set base rates well below forward medical cost trend, that the advance notice for 2027 is “far below” it, and that revisions to the risk-adjustment model have reduced and will continue to reduce funding — a sustained, quantified-by-management policy squeeze on the company’s largest program, arriving while CMS premiums have grown to a record share of consolidated revenue. On Medicaid, management characterizes state funding and payment rates as insufficient to meet patient health needs, is exiting one state, and expects membership losses from reduced eligibility — an explicit statement that a government customer is paying below cost. The pharmacy business faces its own active agenda: the risk factors detail ongoing governmental investigations into PBM practices industry-wide that have already produced civil penalties and corporate integrity agreements, alongside potential legislation on rebates, formularies, pricing benchmarks and network design that could materially change the Optum Rx business model. The Inflation Reduction Act has already shifted more Part D risk onto plans. Layered over all of it sits the disclosure gap on the DOJ Medicare-billing investigations treated as Risk 1 — the defining regulatory fact of this filing year. §

On the social and data dimensions, the company’s obligations are structural rather than reputational: it is one of the largest custodians of protected health information in the country, operating as both covered entity and business associate under HIPAA, and the Change Healthcare breach demonstrated the tail — mass compromise of personal health data at a recently acquired, incompletely integrated business, with provider-loan losses still being reserved nearly two years later and the breach-litigation exposure unquantified in the contingencies footnote. The cybersecurity item describes a credible governance apparatus — NIST-framework alignment, penetration and recovery testing, Board oversight delegated to the Audit and Finance Committee with an external incident-response firm engaged — but its assertion that no cybersecurity threats materially affected the company as of year-end sits awkwardly beside the same filing’s fourth-quarter cyberattack reserve, and we weight the reserve over the assertion. The company also flags its expanding use of AI in operations and products as a legal and regulatory risk in its own right, with health-data and AI legislation evolving at federal and state level — relevant for a business whose moat is explicitly data-driven. On environment, the filing’s exposure is through medical costs rather than operations: management identifies natural disasters and effects of climate change as drivers of increased care costs, a channel that runs straight into the underwriting risk in Section 2.1 rather than into a sustainability report. On governance, three facts from the filing stand on their own: the Chair and CEO roles were recombined in the May 2025 transition, reversing the prior separation; the majority of listed executive officers are new or newly in role within roughly twelve months; and shareholder suits entered the litigation disclosure for the first time. Each is a fact, not an allegation — but together they mean governance execution must be monitored rather than assumed during precisely the period when the financial risks above are most live.

Section 3 — Financial Analysis & Historical Performance

sources Three-Statement Linkage Confirmation: - Net Income ties (Income Statement → Cash Flow Statement): Confirmed. The cash flow statement opens from consolidated net earnings including noncontrolling interests, which reconciles to net earnings attributable to common shareholders after deducting the noncontrolling-interest share. No discrepancy. - Cash ties (Balance Sheet → Cash Flow Statement): Confirmed. Year-end cash and equivalents on the balance sheet tie to the cash flow statement’s ending cash balance in each year of the five-year window. - Retained Earnings reconciliation: Confirmed with one structural note. Beginning retained earnings plus net earnings less dividends does not arrive at ending retained earnings on its own, because the company allocates share-repurchase consideration in excess of par against retained earnings. Once that allocation is incorporated, the account reconciles. The analytically important consequence — disclosed in the forensic review — is that in the most recent year dividends plus buybacks exceeded net earnings attributable to shareholders, and retained earnings declined for the first time in the coverage window.

3.1A Income Statement

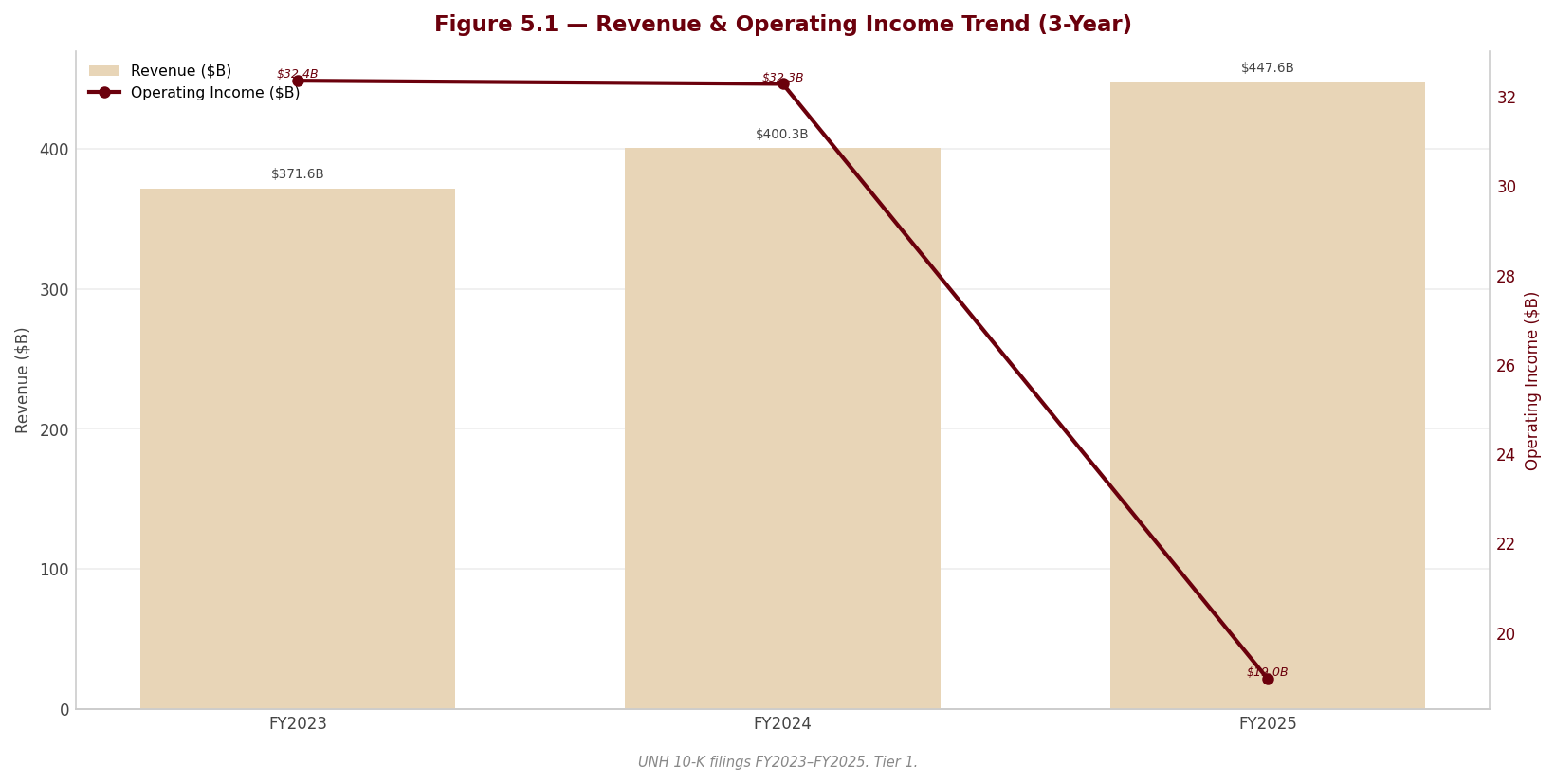

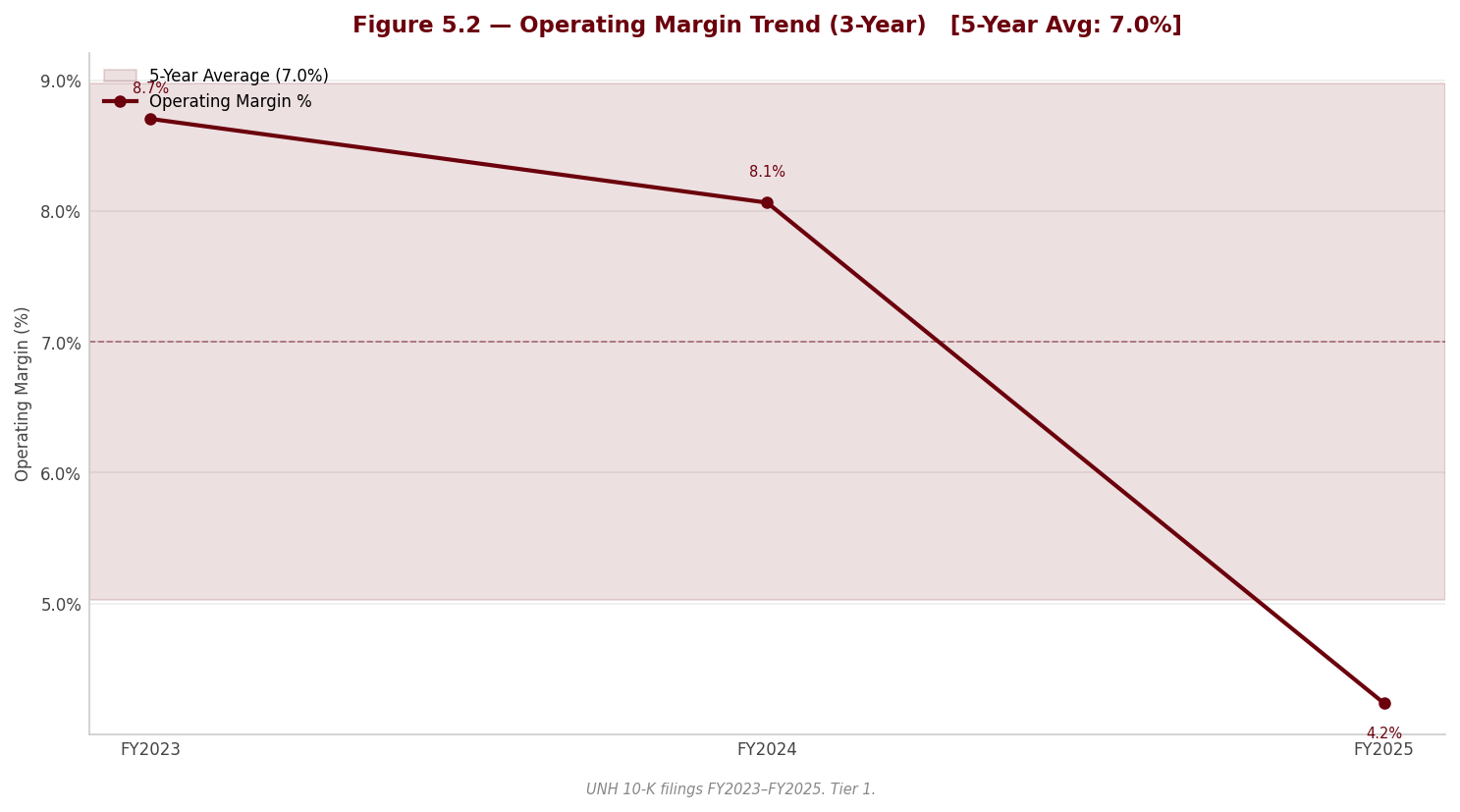

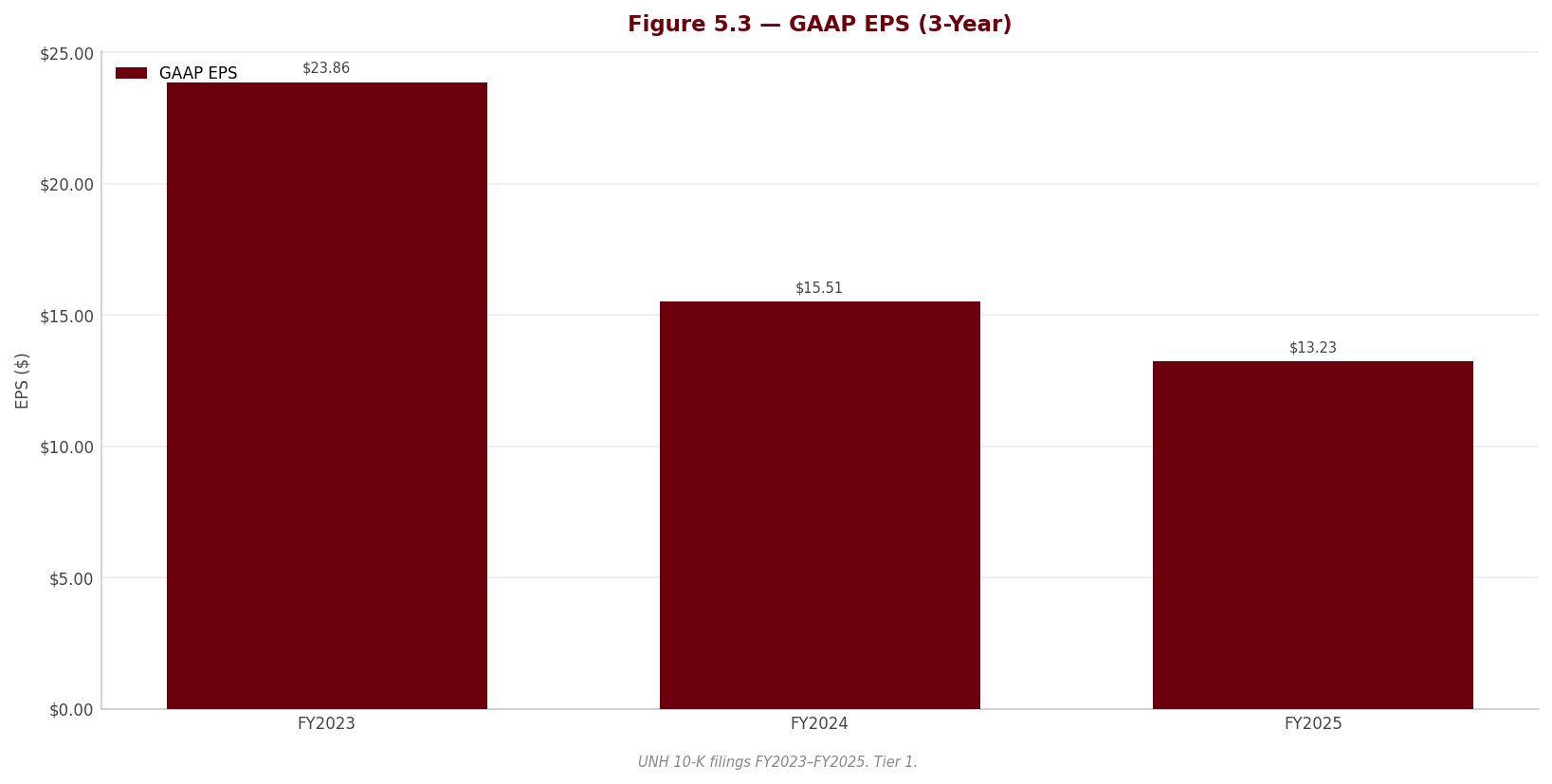

sources | | FY2021 | FY2022 | FY2023 | FY2024 | FY2025 | |—|—|—|—|—|—| | Revenue ($M) | $287,597.0M | $324,162.0M | $371,622.0M | $400,278.0M | $447,567.0M | | YoY Growth | — | 12.7% | 14.6% | 7.7% | 11.8% | | D&A ($M) | $3,103.0M | $3,400.0M | $3,972.0M | $4,099.0M | $4,361.0M | | EBITDA ($M) (computed: EBIT + D&A) | $27,073.0M | $31,835.0M | $36,330.0M | $36,386.0M | $23,325.0M | | EBITDA Margin | 9.4% | 9.8% | 9.8% | 9.1% | 5.2% | | EBITDA Growth | — | 17.6% | 14.1% | 0.2% | -35.9% | | EBIT ($M) | $23,970.0M | $28,435.0M | $32,358.0M | $32,287.0M | $18,964.0M | | EBIT Margin | 8.3% | 8.8% | 8.7% | 8.1% | 4.2% | | Interest Expense ($M) | $1,660.0M | $2,092.0M | $3,246.0M | $3,906.0M | $4,002.0M | | Pre-Tax Income ($M) | $22,310.0M | $26,343.0M | $29,112.0M | $20,071.0M | $14,697.0M | | Tax Expense ($M) | $4,578.0M | $5,704.0M | $5,968.0M | $4,829.0M | $1,890.0M | | Effective Tax Rate | 20.5% | 21.7% | 20.5% | 24.1% | 12.9% | | Net Income ($M) | $17,285.0M | $20,120.0M | $22,381.0M | $14,405.0M | $12,056.0M | | Net Margin | 6.0% | 6.2% | 6.0% | 3.6% | 2.7% | | Net Income Growth | — | 16.4% | 11.2% | -35.6% | -16.3% | | Diluted EPS | $18.08 | $21.18 | $23.86 | $15.51 | $13.23 | | EPS Growth | — | 17.1% | 12.7% | -35.0% | -14.7% | | Diluted Shares (M) | 956 | 950 | 938 | 929 | 911 |

Source: Company FY2025 Form 10-K, consolidated statements of operations; FY2021–FY2023 figures per the corresponding prior-year filings. UnitedHealth reports as an insurer — medical costs and operating costs replace the conventional COGS/gross-profit presentation, so no gross-margin line is shown.

CAGR Summary

| Metric | 3Y CAGR | 5Y CAGR | 10Y CAGR |

|---|---|---|---|

| Revenue | 11.4% | — | — |

| EBITDA | -9.8% | — | — |

| Net Income | -15.7% | — | — |

| Diluted EPS | -14.5% | — | — |

| FCF | -11.8% | — | — |

3.1B Income Statement — Analysis

sources The revenue story. The top line grew every year of the window, from $287,597.0M in FY2021 to $447,567.0M in FY2025, a 11.4% three-year CAGR. But the composition of that growth deteriorated meaningfully in the final year. FY2025’s 11.8% expansion was driven by Medicare Advantage membership growth, higher-acuity Medicaid members, Optum Rx script volume from new and existing clients — and, critically, by the Inflation Reduction Act’s redesign of Medicare Part D, which shifted more risk to plans and mechanically grossed up both premiums and medical costs. Revenue that arrives pre-matched with an equal-and-offsetting cost increase is low-quality growth: it inflates the denominator of every margin ratio without adding profit dollars. The FY2024 deceleration to 7.7% reflected the Change Healthcare cyberattack’s disruption of Optum Insight and the South American divestiture program; the FY2025 reacceleration is therefore partly optical. Looking forward, management guides to membership contraction across Medicare Advantage, Medicaid and value-based care lives — meaning FY2026 is explicitly framed as a shrink-to-restore-margin year, and the five-year pattern of uninterrupted double-digit-average growth should not be extrapolated.

The margin trajectory. This is the center of the investment debate, and management’s own words frame it: the filing concedes that FY2025 pricing and health-status assumptions fell “well short” of the medical cost trend actually incurred, significantly impacting earnings. EBIT margin held in a tight band from 8.3% in FY2021 to a peak of 8.8% in FY2022, eased to 8.1% in FY2024, then collapsed to 4.2% in FY2025 — roughly half the level the franchise sustained for the prior four years. The compression is a layered phenomenon: multi-year Medicare Advantage rate notices set below forward medical cost trend, the phase-in of risk-adjustment model revisions reducing funding, elevated utilization and provider billing intensity, the adverse member profile of newly added value-based care patients, individual-exchange market morbidity, and the Part D risk shift. Our judgment is that the trajectory is part cyclical, part structural: the underwriting miss is repriceable through the FY2026 cycle, but the government-funding squeeze and the disappearance of the reserve-release cushion (below) are structural features of the next several years, not a one-year air pocket.

Major Movers. Five drivers materially moved the income statement, and they must be separated to see the underlying business:

- The underwriting miss (structural-cyclical hybrid). EBIT fell from $32,287.0M to $18,964.0M as medical costs outran priced assumptions across Medicare Advantage, Medicaid and the exchanges. Management has now mis-forecast trend for two consecutive pricing cycles, which weakens confidence in the FY2026 repricing thesis even as benefit-design and county-exit levers are pulled.

- The Q4 “kitchen-sink” restructuring charge (temporary, but read it skeptically). The fourth quarter absorbed a restructuring bundle that the forensic review flags as far broader than conventional restructuring: real-estate rationalization and workforce reductions, but also net valuation losses on equity securities, a discretionary advance funding of the company’s charitable foundation, and — most importantly — a loss contract reserve that pulls anticipated FY2026 value-based care losses into FY2025. This is a classic big-bath pattern in the first full quarter under a new CEO and CFO: it depresses the transition year and manufactures an easier comparison base. Any FY2026 margin “recovery” must be read net of reserve releases and the non-recurrence of these charges.

- A non-cash deconsolidation gain booked inside operating costs (one-off, flattering). A change in governance rights triggered deconsolidation of a business whose redeemable noncontrolling-interest carrying value exceeded its net assets, producing a large gain recorded within operating costs — the principal driver of the net portfolio-action gain attributed to Optum Rx and therefore of that segment’s reported earnings growth. No cash was received; the retained stake is now a Level 3 equity-method investment. Reported FY2025 EBIT is thus simultaneously depressed by the restructuring bundle and inflated by this gain — neither belongs in a run-rate.

- The evaporation of favorable reserve development (structural). Favorable prior-year medical-reserve development has declined sharply for three consecutive years and is now a small fraction of its earlier level, while premium-deficiency and loss-contract reserves appear in the claims rollforward for the first time. The cushion of conservatism that historically released into each year’s earnings is essentially gone: the reported medical care ratio is now a “truer” — and structurally higher — number, with far less buffer if claims trend deteriorates again.

- The tax-rate collapse (unsustainable cushion to net income). The effective rate fell to 12.9% from 24.1% as permanent items — primarily Irish rate differential and Luxembourg tax attributes — plus nontaxable divestiture effects landed on a depressed pre-tax base of $14,697.0M. Without it, the -16.3% net income decline would have been markedly worse. Gross unrecognized tax benefits jumped sharply with IRS examinations open across multiple years; the forward model should normalize toward the historical rate near 20.5%.

A sixth driver compounds below the operating line: interest expense climbed from $1,660.0M to $4,002.0M across the window as debt was added — a structural increase that arrived precisely as the operating earnings supporting it halved.

Quality of earnings. Neither of the last two fiscal years is a clean base. FY2024 carried portfolio-refinement gains in operating results, cyberattack-related provider accommodation costs, and the Brazil divestiture loss below the operating line — which is why FY2024’s effective rate of 24.1% was elevated by non-deductible disposition losses while FY2025’s 12.9% was depressed by their mirror image. FY2025 EBIT of $18,964.0M nets a kitchen-sink charge (including next year’s pre-booked losses) against a non-cash accounting gain. The honest characterization is that underlying FY2025 operating earnings sit somewhere between the reported figure and the FY2024 level, and that the -9.8% three-year EBITDA CAGR overstates the decay in the franchise while the reported FY2025 margin understates its run-rate earning power. Both distortions are disclosed; neither is quantifiable from the face of the statements alone — which is itself a disclosure-quality criticism. One further earnings-quality point carries a forensic RED flag and must be stated plainly: the publicly confirmed Department of Justice criminal and civil investigations into the company’s Medicare billing practices are addressed in the filing only through generic language, with no liability accrued and no range of loss provided. Reported earnings therefore carry no reserve whatsoever for this exposure — any settlement, penalty or program consequence would be entirely incremental to every figure in the tables above. The exposure itself is treated in depth in Section 2; its earnings-quality implication belongs here.

⚠ Items to Watch. - If FY2026 EBIT margin fails to recover meaningfully above 4.2% despite the repricing cycle, the loss-reserve release tailwind and the non-recurrence of the Q4 charge, the structural-impairment thesis displaces the cyclical-trough thesis. - If the effective tax rate remains below 20.5% in FY2026, earnings quality concerns deepen — the historical rate, not the FY2025 print, is the right modeling anchor. - If revenue growth in FY2026 exceeds 7.7% despite guided membership contraction across MA, Medicaid and value-based care, interrogate whether growth is again arriving via the low-quality Part D gross-up channel rather than profitable lives. - Watch the cadence of loss-contract reserve releases against FY2026 medical costs: margin improvement funded by reserve release is accounting, not recovery. - The segment realignment effective at the start of FY2026 — Optum Financial moves from loss-making Optum Health into Optum Insight, with prior periods recast — breaks segment comparability at exactly the moment segment trends matter most; recast figures should be checked for whether they mask underlying deterioration in either segment, particularly given that intersegment transactions are priced at management’s estimate of fair value.

3.2A Balance Sheet

sources | | FY2021 | FY2022 | FY2023 | FY2024 | FY2025 | |—|—|—|—|—|—| | ASSETS | | | | | | | Cash & Equivalents ($M) | $21,375.0M | $23,365.0M | $25,427.0M | $25,312.0M | $24,365.0M | | Receivables ($M) | $14,216.0M | $17,681.0M | $21,276.0M | $22,365.0M | $23,018.0M | | Total Current Assets ($M) | $61,758.0M | $69,069.0M | $78,437.0M | $85,779.0M | $90,582.0M | | PP&E, net ($M) | $8,969.0M | $10,128.0M | $11,450.0M | $10,553.0M | $10,762.0M | | Goodwill & Intangibles ($M) | $75,795.0M | $93,352.0M | $103,732.0M | $106,734.0M | $110,499.0M | | Total Assets ($M) | $212,206.0M | $245,705.0M | $273,720.0M | $298,278.0M | $309,581.0M | | LIABILITIES & EQUITY | | | | | | | Short-term Debt ($M) | $3,620.0M | $3,110.0M | $4,274.0M | $4,545.0M | $6,069.0M | | Total Current Liabilities ($M) | $78,292.0M | $89,237.0M | $99,054.0M | $103,769.0M | $114,897.0M | | Long-term Debt ($M) | $42,383.0M | $54,513.0M | $58,263.0M | $72,359.0M | $72,320.0M | | Total Debt ($M) | $46,003.0M | $57,623.0M | $62,537.0M | $76,904.0M | $78,389.0M | | Net Debt ($M) | $24,628.0M | $34,258.0M | $37,110.0M | $51,592.0M | $54,024.0M | | Total Liabilities ($M) | $135,727.0M | $159,358.0M | $174,801.0M | $195,687.0M | $207,883.0M | | Shareholders’ Equity ($M) | $71,760.0M | $77,772.0M | $88,756.0M | $92,658.0M | $94,110.0M | | Retained Earnings ($M) | $77,134.0M | $86,156.0M | $95,774.0M | $96,036.0M | $95,603.0M | | Key Ratios | | | | | | | Current Ratio | 0.8x | 0.8x | 0.8x | 0.8x | 0.8x | | Net Debt / EBITDA | 0.9x | 1.1x | 1.0x | 1.4x | 2.3x | | Debt / Equity | 0.6x | 0.7x | 0.7x | 0.8x | 0.8x | | Book Value / Share | $75.06 | $81.87 | $94.62 | $99.74 | $103.30 |

Source: Company FY2025 Form 10-K, consolidated balance sheets; prior years per the corresponding filings. As an insurer, the company carries no inventory; inventory-linked working-capital metrics (DIO, cash conversion cycle) are undefined and omitted. Total liabilities are as printed in the filing; note that redeemable noncontrolling interests sit in a mezzanine caption between liabilities and equity, so total liabilities plus shareholders’ equity does not sum to total assets without it.

3.2B Balance Sheet — Analysis

sources Asset composition. This is an acquisition-built balance sheet wearing an insurer’s working-capital structure. Goodwill and intangibles of $110,499.0M dominate total assets of $309,581.0M — by far the largest single asset category — while net PP&E is just $10,762.0M. The company does not build; it buys, and the goodwill stack grew every year of the window, from $75,795.0M in FY2021. The forensic review attaches a RED flag here that we regard as the balance sheet’s most important single issue: Optum Health’s goodwill — the largest of the four segments’ — increased through acquisitions in the same year that segment swung to an operating loss and required a loss-contract reserve for its forward book. Management asserts the annual impairment test found fair values “substantially in excess” of carrying values, but discloses no quantitative headroom, discount rates or growth assumptions — an untestable assertion that sits uneasily beside realized remeasurement losses on the businesses the company actually moved to held-for-sale, where exit values came in below carrying values. If value-based care economics do not recover on the FY2026 repricing, impairment risk migrates from theoretical to live, and a charge would land directly on the equity base supporting credit ratings already carrying negative outlooks. A further structural note: a redeemable noncontrolling-interest balance sits in the mezzanine, outside both liabilities and equity as presented in the table above; that mezzanine balance collapsed year-over-year, driven by the same governance-rights deconsolidation that produced the operating-cost gain discussed in 3.1B.

Leverage trajectory. Total debt grew from $46,003.0M to $78,389.0M and net debt from $24,628.0M to $54,024.0M — a steady, acquisition-funded build that was unremarkable while EBITDA grew alongside it. The FY2025 earnings collapse changed the arithmetic abruptly: net debt/EBITDA jumped from 1.0x in FY2023 to 1.4x in FY2024 and 2.3x in FY2025, with gross debt/equity reaching 0.8x. The deterioration is denominator-driven, but the consequences are real, and the forensic memo’s holding-company findings sharpen them considerably: in FY2025 the regulated insurance subsidiaries — historically the engine that up-streamed billions in dividends to the parent — instead received net capital infusions, the parent’s borrowings from its own subsidiaries rose materially, and the company entered reinsurance agreements under deposit accounting (no risk transfer) to manage statutory surplus. That combination — subsidiaries absorbing capital, intercompany funding of external obligations, and capital engineering via reinsurance — is the signature of a holding company whose internal cash engine has temporarily reversed. Required statutory capital is expected to increase further as the elevated medical care ratio flows through. No covenant breach is flagged, but deleveraging, buyback resumption and dividend growth all now depend on the medical care ratio normalizing. One off-balance-sheet item belongs in any complete leverage picture: the portfolio-refinement program left the company holding minority stakes in unconsolidated businesses with newly quantified put and call options attached — a multi-billion-dollar estimated redemption obligation if currently redeemable, disclosed for the first time this year, that appears nowhere among the liabilities in the table above. The puts are largely counterparty-controlled and sit outside the next twelve months, but they are a potential future call on the same parent liquidity already under strain.

Working capital. A current ratio of 0.8x — below parity in every year shown — would alarm in an industrial context but is structural for an insurer: premiums are collected before claims are paid, and the resulting float is the business model, not a liquidity defect. The receivables picture deserves more scrutiny than the headline suggests. DSO improved to 19 days in FY2025 from 20 days in FY2024, which would ordinarily read as collection discipline — but the forensic review identifies a new, uncommitted, sub-one-year receivables-sale facility entered during FY2025, under which sold receivables are derecognized and the proceeds classified as operating cash flow. Part of the apparent receivables improvement is therefore monetization, not collection, and it can reverse if the banks decline to renew. Receivables of $23,018.0M nonetheless grew more slowly than revenue in FY2025, so there is no adverse build signal beyond the facility caveat. One watch item within the receivables base: nearly two years after the Change Healthcare cyberattack, the company took a sizable incremental reserve against collection of the interest-free loans it extended to affected care providers, and the allowance on other current receivables rose markedly year-over-year — a live, slow-burning credit tail from that event, absorbed in Optum Insight’s results.

⚠ Items to Watch. - If net debt/EBITDA remains above 1.4x at FY2026 year-end — i.e., fails to retrace even to the FY2024 level as earnings recover — the negative rating outlooks become live downgrade risk and the capital-return program stays constrained. - Any Optum Health goodwill impairment charge against the $110,499.0M goodwill-and-intangibles stack is a direct hit to the $94,110.0M equity base; watch the FY2026 annual test disclosure for the first appearance of quantified headroom. - If regulated subsidiaries require net capital infusions for a second consecutive year, parent-level dividend capacity is the binding constraint — regardless of consolidated earnings. - A reversal of the receivables-sale facility would show up as a working-capital drag; watch whether DSO retraces toward 20 days.

3.3A Cash Flow Statement

| FY2021 | FY2022 | FY2023 | FY2024 | FY2025 | |

|---|---|---|---|---|---|

| Cash from Operations ($M) | $22,343.0M | $26,206.0M | $29,068.0M | $24,204.0M | $19,697.0M |

| Capital Expenditures ($M) | $-2,454.0M | $-2,802.0M | $-3,386.0M | $-3,499.0M | $-3,622.0M |

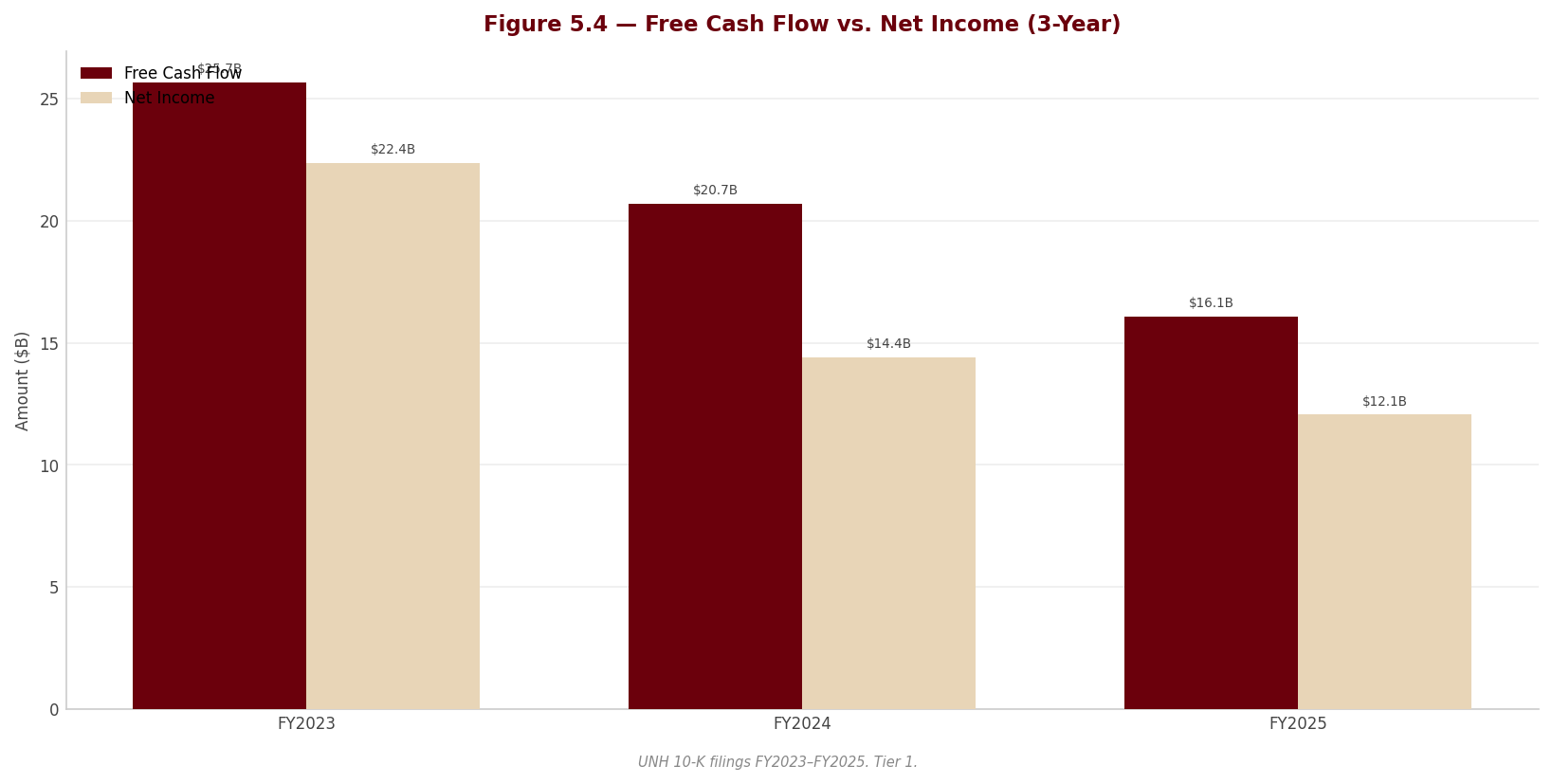

| Free Cash Flow ($M) | $19,889.0M | $23,404.0M | $25,682.0M | $20,705.0M | $16,075.0M |

| FCF Margin | 6.9% | 7.2% | 6.9% | 5.2% | 3.6% |

| FCF / Share | $20.80 | $24.64 | $27.38 | $22.29 | $17.65 |

| FCF Conversion (FCF/NI) | 115.1% | 116.3% | 114.7% | 143.7% | 133.3% |

| CapEx / Revenue | 0.9% | 0.9% | 0.9% | 0.9% | 0.8% |

| CapEx / D&A | 0.8x | 0.8x | 0.9x | 0.9x | 0.8x |

| Dividends Paid ($M) | $-5,280.0M | $-5,991.0M | $-6,761.0M | $-7,533.0M | $-7,916.0M |

| Share Repurchases ($M) | $-5,000.0M | $-7,000.0M | $-8,000.0M | $-9,000.0M | $-5,545.0M |

Source: Company FY2025 Form 10-K, consolidated statements of cash flows; prior years per the corresponding filings.

3.3B Cash Flow — Analysis

sources Quality of operating cash flow. Operating cash flow peaked at $29,068.0M in FY2023 and has declined for two consecutive years, to $24,204.0M and then $19,697.0M — a -9.1% three-year CAGR. Headline FCF conversion looks excellent at 133.3%, but that figure flatters for two reasons and must not be read as a quality signal. First, the denominator: net income is depressed by the non-cash Q4 charges, so conversion above one hundred percent is partly an artifact of the same charges that crushed earnings — the FY2024 reading of 143.7% carries the identical distortion in reverse direction from the Brazil loss. Second, the numerator: per the forensic review, FY2025 operating cash flow was explicitly supported by the new receivables-sale facility — management itself lists the sale of receivables among the supports to the year’s operating cash flows. Because the facility is uncommitted and matures inside a year, that benefit is borrowed, not earned; non-renewal converts it into an FY2026 operating-cash-flow headwind. Management separately states the net FY2026 cash impact of the restructuring actions should be immaterial — accrual outflows offset by disposal proceeds — which confirms the Q4 charges were largely non-cash or timing in nature, consistent with the big-bath reading in 3.1B. Adjusting mentally for the facility, underlying FY2025 cash generation declined materially but remained solidly positive; the franchise still throws off cash even in its worst underwriting year in the window.

CapEx analysis. Capital intensity is structurally trivial and stable: CapEx runs below one percent of revenue (0.8% in FY2025) and has sat below parity with depreciation throughout the window (0.8x in FY2025). For an industrial, a sub-1.0x CapEx/D&A ratio would suggest harvest mode; here it simply reflects where growth capital actually goes — acquisitions, which bypass the CapEx line entirely and accumulate as the goodwill stack analyzed in 3.2B. The filing does not split maintenance from growth CapEx; given the magnitudes, the distinction is immaterial to valuation. The real reinvestment question for this company is M&A discipline, not CapEx sufficiency.

Capital allocation waterfall. Over the five years shown, cumulative FCF was absorbed roughly equally by shareholder returns and by acquisition spending funded alongside debt issuance. Within shareholder returns the mix is shifting in a direction that warrants attention. Dividends rose every single year, from $-5,280.0M to $-7,916.0M, and the payout ratio has climbed from 30.5% to 65.7% — driven by the earnings collapse, not by a policy change, but a payout at that level on depressed earnings consumes flexibility. Buybacks tell the sharper story: repurchases peaked at $-9,000.0M in FY2024, were cut to $-5,545.0M in FY2025, and — per the forensic review — stopped entirely in the closing months of the year, after the full-year repurchases had been executed at an average price far above where the stock ended the year. Value-destructive timing followed by a halt, alongside a mid-year dividend increase, reads as capital conservation forced by the holding-company strain documented in 3.2B rather than as opportunism. The net result, flagged in the linkage confirmation above: dividends plus buybacks exceeded attributable net earnings, and retained earnings fell from $96,036.0M to $95,603.0M. Per-share support from repurchases — the diluted count fell at a -1.4% three-year CAGR to 911M — should not be assumed to continue in FY2026.

⚠ Items to Watch. - If FY2026 operating cash flow falls below the FY2025 level of $19,697.0M, the decline is worse than it appears — the FY2025 base already includes the one-time receivables-facility benefit. - If the dividend payout ratio remains above 52.3% in FY2026, the dividend-growth streak is colliding with the earnings base; a payout retracing toward 30.2% on recovered earnings is the healthy path. - Buyback resumption ahead of visible subsidiary-dividend normalization would be a yellow flag for capital discipline, not a bullish signal. - FCF/share below $17.65 for a second year would force the dividend conversation: DPS of $8.69 already consumes roughly half of FY2025 FCF per share.

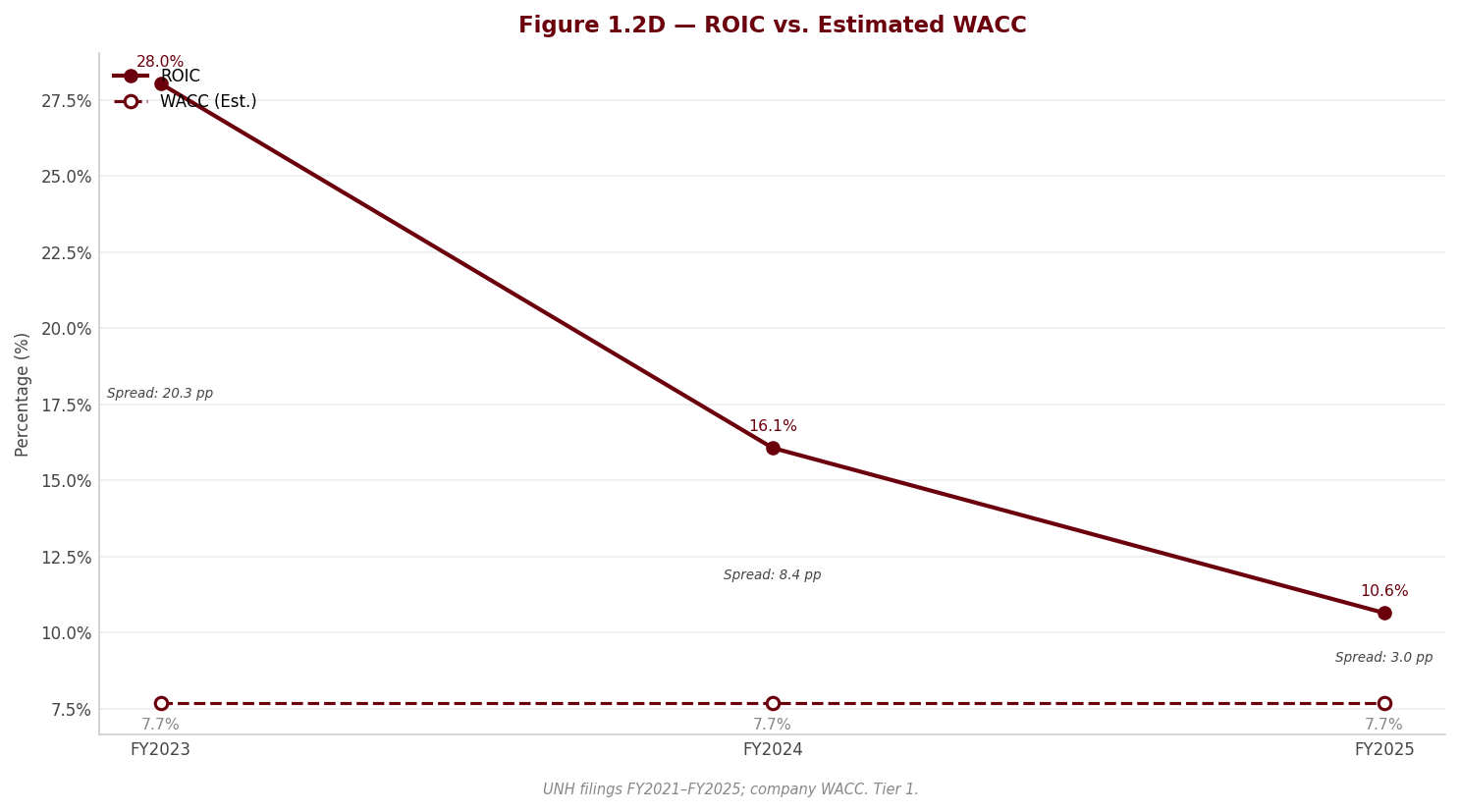

3.4 Returns Analysis

sources | | FY2021 | FY2022 | FY2023 | FY2024 | FY2025 | |—|—|—|—|—|—| | ROIC | 19.8% | 21.4% | 21.6% | 18.2% | 11.3% | | ROE | 24.1% | 26.9% | 26.9% | 15.9% | 12.9% | | ROA | 8.1% | 8.8% | 8.6% | 5.0% | 4.0% | | Interest Coverage | 14.4x | 13.6x | 10.0x | 8.3x | 4.7x |

The returns table is the cleanest summary of what FY2025 did to this franchise. ROIC peaked at 21.6% in FY2023 — an elite figure for a business of this scale, and the quantitative expression of the flywheel described in Section 1 — then fell to 18.2% and 11.3%. Even the depressed FY2025 figure should remain above the cost of capital derived in Section 4, meaning the company is still creating value on its invested base at the trough — but the spread has compressed from commanding to ordinary in two years. The decomposition matters: invested capital kept growing (the goodwill build of 3.2B) while NOPAT halved, so the ROIC decline is both a numerator collapse and a denominator that never stopped expanding. The recovery case requires the FY2026 repricing to restore the numerator against a capital base that the company is now actively pruning through divestitures. Interest coverage tells the same story from the creditor’s seat: 14.4x in FY2021 has fallen to 4.7x — still comfortable in absolute terms, but a steep glide path, and the figure embeds the depressed, charge-laden FY2025 EBIT.

The DuPont decomposition isolates where ROE was won and lost. FY2025 ROE of 12.9% decomposes into a net margin of 2.7%, asset turnover of 1.47x and an equity multiplier of 3.25x. Asset turnover is the stable backbone — it actually improved in FY2025 as the Part D gross-up pushed revenue up faster than assets — and the equity multiplier has drifted up only modestly across the window. The entire collapse from the 26.9% FY2023 ROE to 12.9% in FY2025 is therefore a margin event: net margin compressed from 6.0% to 2.7%. The swing factor is, and will remain, the underwriting margin — turnover and leverage are structurally pinned by the business model. This is analytically convenient: the ROE recovery thesis collapses into a single question, which is whether the medical care ratio normalizes, and every margin watch-item in 3.1B applies here without modification.

3.5 Altman Z-Score (Most Recent FY)

sources | Component | FY2023 | FY2024 | FY2025 | |—|—|—|—| | X1 (Working Capital / Total Assets) | -0.075 | -0.060 | -0.079 | | X2 (Retained Earnings / Total Assets) | 0.350 | 0.322 | 0.309 | | X3 (EBIT / Total Assets) | 0.118 | 0.108 | 0.061 | | X4 (Equity / Total Liabilities) | 0.508 | 0.474 | 0.453 | | X5 (Revenue / Total Assets) | 1.358 | 1.342 | 1.446 | | Z-Score | 2.45 | 2.36 | 2.26 | | Zone | Gray (1.81–2.99) | Gray (1.81–2.99) | Gray (1.81–2.99) |

The company sits in the gray zone in all three years shown, and the score has declined in each of the last two — moving toward, not away from, the distress boundary. Two readings must be held simultaneously. First, the model’s mechanics overstate risk for an insurer: X1 is structurally negative because premium float makes negative working capital the business model, not a stress symptom, and the Z-score was calibrated on manufacturers. A gray-zone reading for a large health insurer is normal and carries no implication of distress. Second — and this is the part not to soften — the direction is informative even where the level is not. The deterioration is driven almost entirely by X3, the EBIT-to-assets ratio, which roughly halved in FY2025, with X2 and X4 also eroding as retained earnings declined and liabilities grew. In other words, the model is correctly detecting exactly what the rating agencies’ negative outlooks detect: a profitability shock landing on a balance sheet that kept levering through it. Credit risk here is not solvency risk — it is downgrade risk, with consequences for funding costs and commercial-paper flexibility. A recovery in X3 alongside stabilization of X2 in FY2026 would retrace the score toward its FY2023 level; a third consecutive decline would mean the profitability shock is compounding rather than mean-reverting.

Section 4 — Valuation Methodology

4.1 Cost of Capital (WACC)

sources All inputs to the WACC are verified market data (from market-researcher output) or approved analyst assumptions. Computed metrics are marked accordingly.

4.1.1 Cost of Equity

sources | Component | Value | Source | |—|—|—| | Risk-Free Rate (10Y UST) | 4.55% | US Treasury 10-year par yield | | Equity Risk Premium | 4.18% | Damodaran implied ERP | | Beta (Levered) | 0.65 | 5-year monthly regression — raw, not relevered | | Size Premium | 0.00% | Not applied — mega-cap issuer | | Company-Specific Risk Premium | 2.31% | Analyst judgment — rationale below | | Cost of Equity (Ke) | 8.77% | CAPM: Rf + β × (ERP + CRP) |

The beta of 0.65 is the raw five-year monthly estimate, deliberately not relevered. Total debt has risen meaningfully over the estimation window — from $57,623.0M in FY2022 to $78,389.0M in FY2025 — but market-value leverage remains modest, and relevering off the current market debt-to-equity ratio would be circular: that ratio is elevated primarily because the equity price collapsed in 2025 on idiosyncratic news, not because of a financing decision. The honest caveat cuts the other way as well — the 2025 idiosyncratic drawdown depresses the measured beta, so the regression understates forward-looking risk. That residual risk is addressed explicitly through the company-specific premium rather than by adjusting beta, which keeps the judgment visible in one place instead of buried in a relevering convention.

The company-specific risk premium of 2.31% is the single most consequential judgment in this valuation, and it deserves to be read as exactly that: a discretionary analyst overlay, not a market-derived input. It is applied for three forensic findings that no CAPM input can capture. First, publicly confirmed Department of Justice criminal and civil investigations into Medicare billing practices are carried at zero accrual, with no named disclosure in the filing and no estimable loss range — an unpriced tail against the company’s largest revenue source. Second, holding-company liquidity is strained: regulated subsidiaries are absorbing capital rather than upstreaming dividends, the parent is leaning on intercompany funding, and all three rating agencies carry Negative outlooks. Third, a cluster of earnings- and cash-flow-quality findings — a kitchen-sink fourth-quarter charge, operating cash flow supported by a new uncommitted receivables-sale facility, and an exhausted favorable-development cushion — materially raises forecast risk. Because the workbook formula scales this premium by beta, the input was calibrated to deliver the intended uplift to the cost of equity. Removing the premium entirely would lower the WACC and raise the DCF fair value by more than any other single input change in this report; a reader who rejects the premium should re-derive the valuation before relying on Section 6. Even with the premium, the resulting Ke of 8.77% is not high by broad-market standards — the depressed measured beta dominates the calculation — which is itself a reason the discretionary overlay exists.

4.1.2 Cost of Debt

sources | Component | Value | |—|—| | Pre-tax Cost of Debt (Kd) | 5.15% | | Marginal Tax Rate | 20.50% | | After-tax Cost of Debt | 4.10% |

The pre-tax cost of debt of 5.15% is derived from FY2025 interest expense divided by average total debt across the FY2024 and FY2025 balance sheets, both taken from the Excel workbook. The implied spread over the risk-free rate is modest and consistent with a single-A composite credit profile — but all three agencies hold Negative outlooks, so the realized cost of incremental debt is more likely to drift above this figure than below it if the holding-company strain persists.