Southern Copper Corporation

Section 1 — Business Overview, Operations & Competitive Positioning

1.1 The Business

sources Southern Copper Corporation digs copper out of two of the world’s largest ore systems in Peru and Mexico, processes it through its own smelters and refineries down to refined metal and copper rod, and sells it at prices set by the global commodity market — so the entire economic model rests on producing a price-taking product at a cash cost management believes is among the lowest of any copper producer of comparable size. §

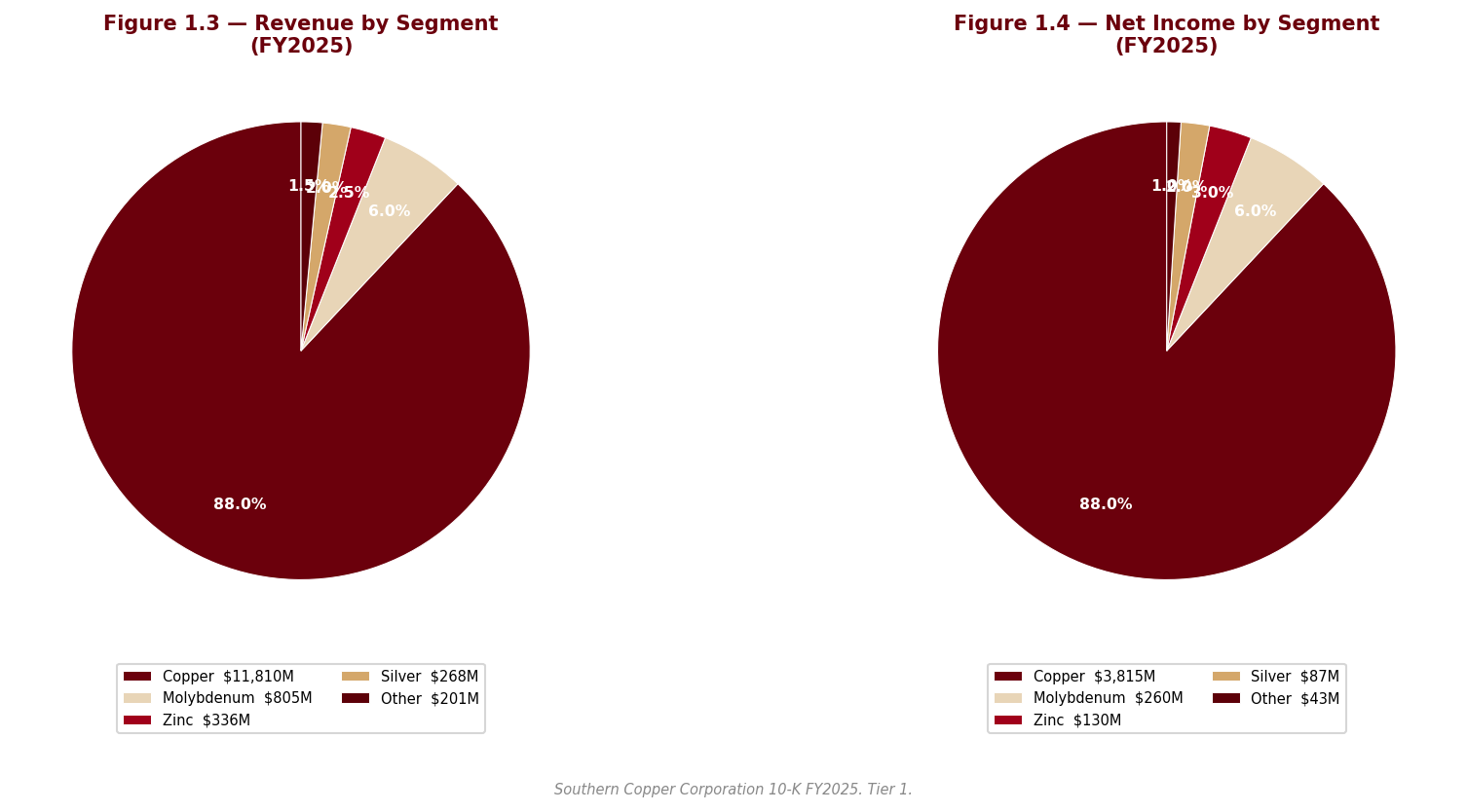

The company is one of the largest integrated copper producers globally, with material by-product output of molybdenum, zinc and silver, and management believes it holds the largest copper reserves in the world. Every mining, smelting and refining asset sits in Peru or Mexico; exploration extends to Argentina and Chile. The business is vertically integrated from ore extraction through refined copper rod, including most of its own transport and logistics — an industrial railroad and port facilities serve the Peruvian mines. Because selling prices are determined by market forces beyond its control, management’s stated operating philosophy is cost control and production enhancement: remain profitable at the bottom of the copper cycle, maximize results at the top. Revenue in the most recent fiscal year reached 13,420.0M, a record, up from 10,934.1M four years earlier and 5,046.0M a decade ago — a trajectory that reflects both copper price cycles and the progressive addition of by-product volume, most recently zinc from the new Buenavista concentrator. The marketing model favors annual and longer-term contracts with end-user customers over spot sales and trading intermediaries, with deliberate diversification by region and customer.

The workforce is majority-unionized in both countries and largely hired locally; in Peru, the company signed long-term extensions of its collective bargaining agreements with all of its unions during the year, with no-stoppage commitments intended to keep operations running normally through at least 2027. The stock has been listed on both the New York and Lima exchanges since 1996. The company is a majority-owned, indirect subsidiary of Grupo Mexico — a structural fact that shapes governance, capital allocation and related-party economics throughout this report.

Key Information

| Item | Value |

|---|---|

| Ticker | SCCO |

| Sector / Industry | Metals & Mining — Copper |

| Report Date | 2026-06-07 |

| Most Recent FY Revenue | 13,420.0M |

| EBIT Margin (Most Recent FY) | 52.2% |

| Diluted Shares (FY2025 weighted avg) | 827M |

Source: verified workbook (SCCO_Portfolio.xlsx), figures traceable via lineage.json to the cited filings.

1.2 Operating Segments

sources Southern Copper reports three segments, which the chief operating decision maker evaluates primarily on operating income and total assets — reviewing production, net sales and operating income variances against budget and prior periods, plus capital expenditure execution, to allocate capital between them. §

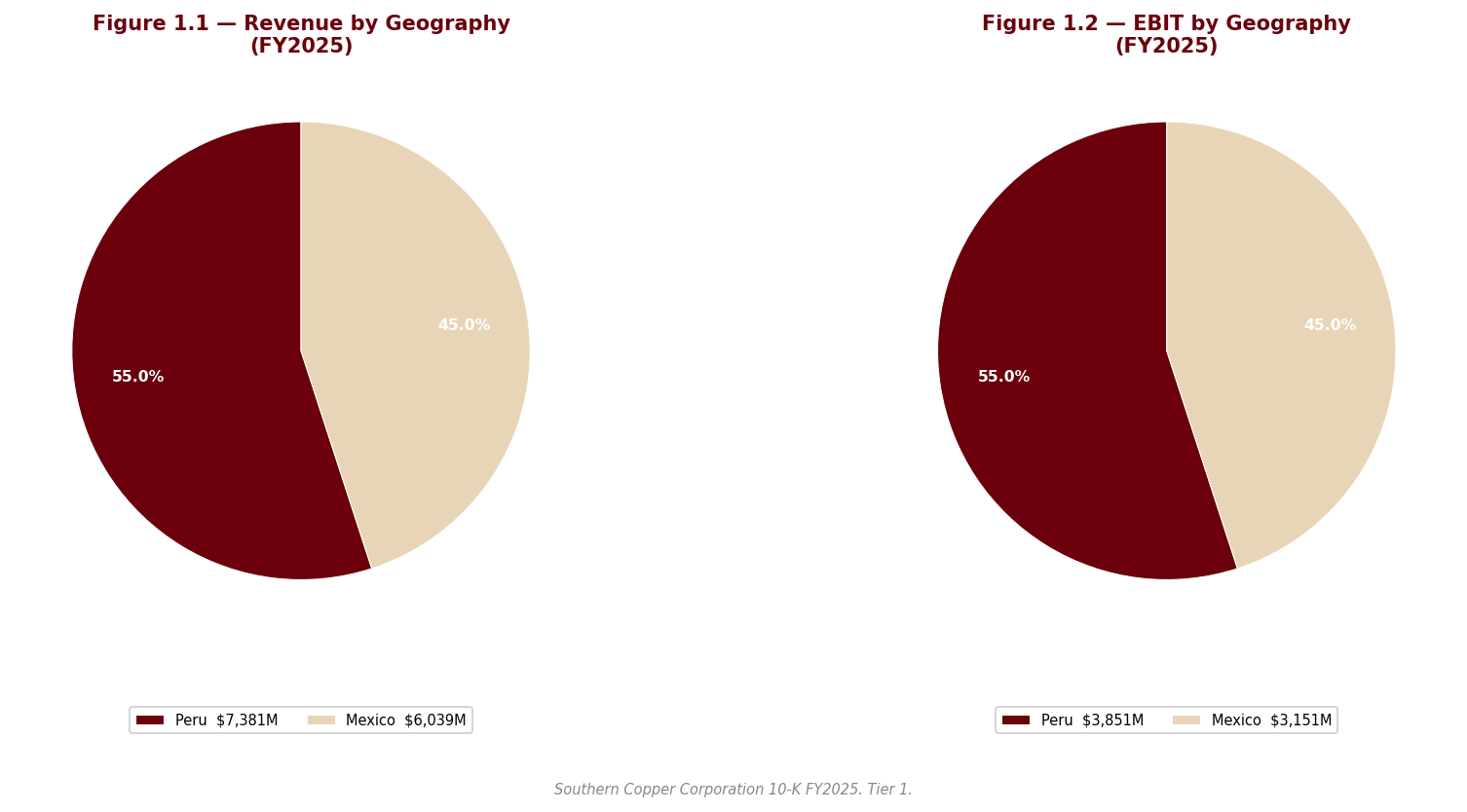

Peruvian operations. The Toquepala and Cuajone open-pit complexes high in the Andes, plus the smelting and refining plants at the coastal city of Ilo — including a precious metals plant, the industrial railroad and port facilities that serve both mines. The segment produces copper with molybdenum and silver by-products, and refined copper via SX-EW. The single variable that drives this segment is the copper price applied to ore grades that declined at both Toquepala and Cuajone in the most recent year — meaning the segment needs either price or the Tia Maria growth project to offset grade-driven volume attrition.

Mexican open-pit. The La Caridad and Buenavista complexes with their smelters, refineries, a precious metals plant, a copper rod plant and shared support facilities. Buenavista sits on one of the world’s largest copper ore deposits. This segment now produces copper and zinc: the new Buenavista zinc concentrator ran at full capacity in the most recent year and was the principal driver of a sharp rise in zinc output, even as copper grades and recoveries at Buenavista weakened with the concentrator dedicated to zinc. The economic driver here has therefore broadened — the segment’s earnings now respond to the zinc price as a meaningful second factor alongside copper.

IMMSA (Mexican underground). Five underground mines producing zinc, copper, lead, silver and gold, together with a zinc refinery. This is the polymetallic tail of the portfolio — small relative to the open-pit segments, with economics driven by zinc and silver prices and by the grade and throughput of the underground operations rather than by copper. One IMMSA asset, the Taxco mine, has been on strike since 2007.

How the system fits together. The flywheel is by-product economics feeding cost leadership: molybdenum, zinc, silver and gold revenue credits absorb a substantial share of fixed costs, pushing the net cash cost of producing a pound of copper toward the bottom of the industry curve. Vertical integration — own smelting, refining, rail and port — captures margin that pure miners surrender to third-party processors and keeps treatment and refining economics in-house. The fragility is the mirror image: all three segments share the same two jurisdictions and, in the open-pit segments, the same primary commodity, so the portfolio offers operational diversification but very little economic diversification. When copper falls, all of it falls together, and the by-product cushion — itself commodity-priced — is correlated rather than offsetting.

1.3 Geographic Exposure

sources The asset base is entirely binational: every producing mine, smelter and refinery is in Peru or Mexico, with exploration extending to Argentina and Chile. Revenue, by contrast, is deliberately diversified by region and customer through the end-user contract model, so geographic risk in this company is asset-side, not demand-side. The company holds extensive mining concessions in both countries — indefinite-term in Peru subject to annual fees, multi-decade renewable terms in Mexico — and generally owns the land and processing facilities outright.

The U.S. dollar is the functional currency and revenue is primarily dollar-denominated, but meaningful portions of operating costs are denominated in Peruvian soles and Mexican pesos; both currencies appreciated against the dollar during the year, a cost headwind that recurs whenever local appreciation outruns local inflation relief. The concentrated jurisdictional footprint carries real political weight: Peru is heading into general elections in April 2026 after a period of acute presidential instability, and Mexico has enacted Mining Law changes and a judicial reform whose effects management itself describes as not currently determinable. These exposures are treated in depth in Section 2; the point for the business overview is that there is no third country to retreat to — the company’s license to operate in exactly two states is the whole franchise.

1.4 Management Team

sources The anchor of this management structure is not an individual executive — it is the controlling shareholder. Grupo Mexico holds a super-majority of the capital stock through its wholly-owned subsidiary Americas Mining Corporation, determines the outcome of substantially all shareholder votes, and shares officers and directors with the company. The filing itself cautions explicitly that the parent’s interests may conflict with those of minority stockholders. Practically, this means strategy, board composition, dividend policy and capital project approval are set by Grupo Mexico, and the public-company management team executes within that mandate. §

The execution record under this structure is, on the operating evidence, disciplined: a consistent multi-decade strategy of cost control and organic growth, no disclosed CEO change during the year, long-dated labor agreements secured in Peru, and a record-revenue, record-net-income year delivered on by-product expansion rather than copper volume. The governance trade-off is equally consistent: extensive related-party purchasing from Grupo Mexico affiliates — including most of the electricity for the Mexican open-pit operations under long-dated contracts with parent-owned generators — operates alongside the conflict-of-interest caution in the filing. The succession and key-person question that matters for most companies is, here, subordinate to a structural one: minority shareholders are permanent passengers in a vehicle steered by the parent. The full governance assessment, including the related-party economics, is in Section 2.

1.5 Capital Allocation Track Record

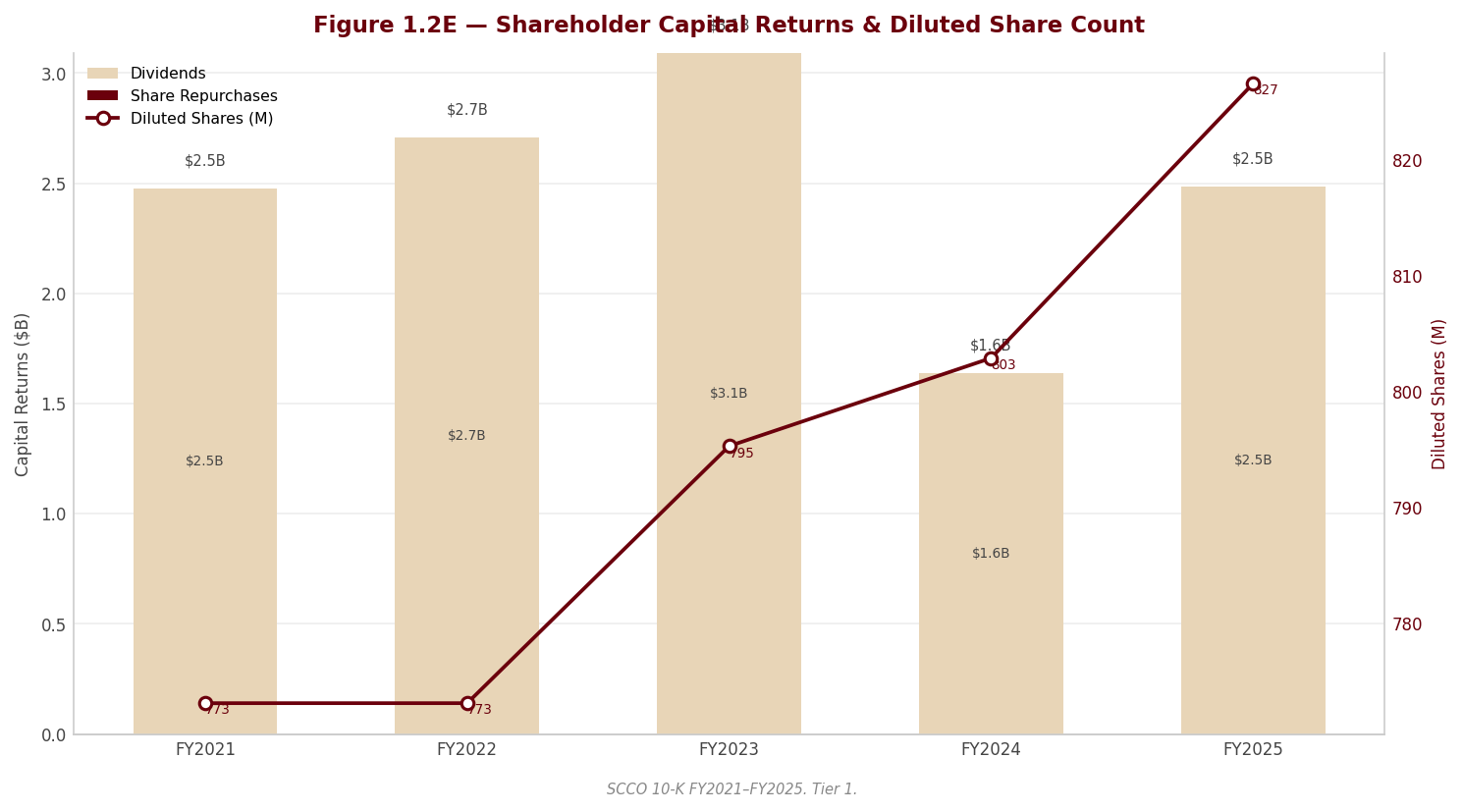

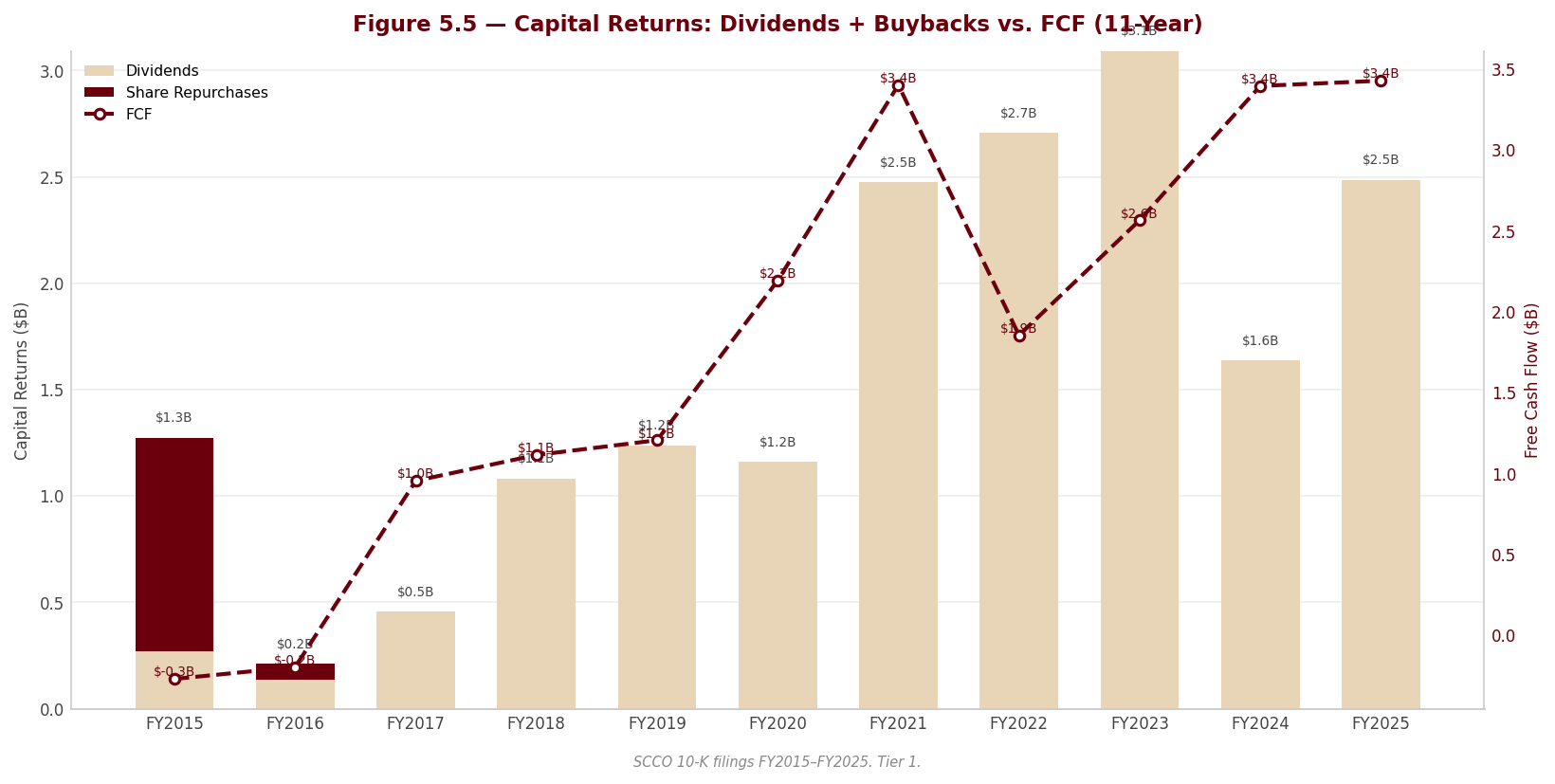

sources Southern Copper’s capital allocation has two simultaneous and unusually large commitments: heavy cash dividends — the company has distributed a significant share of net income as dividends since 1996 — and an expanding organic growth program aimed at substantially higher copper production by 2033. There is no third leg: the share repurchase program, although still authorized with no expiration date, has registered no activity since the third quarter of 2016, and since the second quarter of 2024 the Board has paid quarterly stock dividends out of previously repurchased treasury shares in addition to cash dividends — a mechanism that grows the share count rather than shrinking it.

| Year | Dividends Paid ($M) | Share Repurchases ($M) | CapEx ($M) |

|---|---|---|---|

| FY2021 | -2,473.8M | — | -892.3M |

| FY2022 | -2,705.8M | — | -948.5M |

| FY2023 | -3,092.4M | — | -1,008.6M |

| FY2024 | -1,637.2M | — | -1,027.3M |

| FY2025 | -2,485.1M | — | -1,325.3M |

Source: Company 10-K filings FY2021–FY2025, consolidated statements of cash flows, as compiled in the Data sheet of the SCCO workbook. Share repurchase program inactive since Q3 2016.

The signal in the mix is confidence in the asset base over financial engineering. Capital is being pushed into the business at an accelerating rate: the Board approved an enlarged capital investment program for the coming year, with spending concentrated in the Buenavista tailings facility, the new zinc concentrator, IMMSA mine development and the ramp-up of Tia Maria — the flagship Peruvian project now under construction and targeted for 2027 operations — while management states that Peruvian projects in construction or engineering could absorb a multi-billion-dollar sum over the next decade, with a parallel multi-billion-dollar pipeline under discussion in Mexico. That CapEx is increasingly growth capital rather than replacement capital is the central read: the company is building new production capacity (Tia Maria, the zinc concentrator, El Pilar) on top of maintaining existing operations, not merely sustaining a depleting asset.

Two caveats temper the shareholder-return story. First, the stock-dividend mechanism is dilutive by construction — treasury shares are being handed out rather than retired, expanding the per-share denominator. Second, with Grupo Mexico holding a super-majority of the shares, the overwhelming bulk of every cash dividend flows to the parent; the dividend policy should be read partly as a parent-funding channel, a dynamic the filing’s own risk factors acknowledge and which Section 2 examines in detail. Management’s stated discipline — every project must increase production, decrease costs or address social and environmental commitments — is the right framework; the governance question is who the discipline ultimately serves.

1.6 Competitive Positioning & Moat

sources §1.6.1 Industry structure. Copper is a pure commodity industry: competition is based primarily on price and service, and the filing is explicit that price dominates when supplies are ample. Products also compete with substitute materials, principally aluminum and plastics. In such a structure, no producer has pricing power; returns accrue to whoever sits lowest on the cost curve and owns the longest-lived, highest-quality ore bodies. Position on the cost curve is determined by ore grade, scale, by-product endowment and integration — all asset-level attributes that cannot be replicated quickly, because new world-class copper deposits are scarce, permitting takes decades, and the industry’s main competitors have consolidated into larger, more diversified groups. The cycle, meanwhile, is set by Chinese demand, global inventories and increasingly by trade policy.

§1.6.2 Competitive advantages. Southern Copper’s moat is geological and structural, and each claimed element is anchored in the filing. First, reserves: management believes the company holds the largest copper reserves in the world, with Buenavista alone sitting on one of the world’s largest copper ore deposits — in a depleting industry, reserve life is the scarcest asset. Second, cost position: management states its controllable cash cost is one of the lowest of all copper producers of similar size, explicitly supported by by-product revenue credits from molybdenum, zinc, silver and gold that help cover fixed costs — and the by-product engine grew in the most recent year as the Buenavista zinc concentrator reached full capacity, driving the net unit cash cost down sharply. Third, integration: ownership of the full chain from mine through smelter, refinery, rail and port internalizes processing margin and logistics control that single-stage competitors must buy. Fourth, tenure: concessions in Peru carry indefinite terms and the company generally owns its land and facilities, while long-term collective bargaining agreements in Peru lock in labor peace into 2027. None of these advantages confers pricing power — they confer survivability at the bottom of the cycle and superior cash conversion at the top, which is the only durable form of advantage available in this industry.

§1.6.3 Competitive vulnerabilities. The vulnerabilities are as structural as the strengths. The company is a price-taker on effectively its entire revenue base, and its by-product cushion is itself commodity-priced. Ore grades are declining at the core Peruvian pits and at Buenavista’s copper circuit — the most recent year’s copper production fell on grades, and management guides lower copper output again for the coming year — so the existing asset base is on a slow treadmill that only the project pipeline can reverse. That pipeline is exposed to the company’s deepest weakness: social license in exactly two jurisdictions. Tia Maria was delayed for years by community opposition before construction finally advanced; Los Chancas is currently blocked by illegal miners occupying the project area; Taxco has been on strike since 2007; and violent protests at Cuajone in 2022 halted production. Layer on Peruvian political instability heading into the April 2026 elections, Mexican Mining Law and judicial reform whose effects management cannot quantify, new U.S. tariffs on semi-finished copper products, and a controlling shareholder whose interests may diverge from the float, and the moat’s perimeter is clear: nothing erodes the ore body, but plenty can interdict access to it.

§1.6.4 Verdict. Southern Copper holds a genuine, asset-based moat — reserve scale, by-product-subsidized cost leadership and full integration — of the only kind that matters in a commodity industry, and it should keep the company profitable through the trough of any plausible copper cycle. But the moat protects margins against competitors, not against the copper price, and not against the political and community risk concentrated in its two host countries. Long-run margin durability is therefore a two-variable bet: the cost-curve position looks defensible for as long as the by-product engine and grades hold, while the realized margin will swing with copper and with Peru’s and Mexico’s tolerance for large-scale mining. Investors are buying the best seat in a theater they do not control.

Section 2 — Key Risks & Catalysts

2.1 Downside Risks

sources The risk landscape at Southern Copper is dominated not by the commodity cycle — which every copper producer shares — but by governance: a super-majority controlling shareholder whose commercial relationships with the company are extensive, growing, and verified as arm’s-length only by the company’s own internal processes. Around that core sit a newly escalated legal exposure in Peru, an earnings base partly marked to a near-record copper price, a project pipeline hostage to social license in two countries, and a Mexican fiscal regime whose direction of travel is unambiguously tighter.

The Grupo Mexico relationship — minority shareholders inside a controlled vehicle

sources This is the highest-priority risk in the filing, and the forensic review of the related-party footnote flags it as a red-level governance concern. Grupo Mexico, through its wholly-owned subsidiary Americas Mining Corporation, holds a super-majority of the capital stock and determines the outcome of substantially all shareholder votes — board composition, dividends, capital projects, asset sales. The commercial web around that control is extensive: administrative, legal and treasury services, rail freight, construction, engineering, captive power for the Mexican operations from three parent-owned generators under contracts running to 2032 and, in one case, two decades, metal purchases and tolling from sister company Asarco, and aviation and entertainment services from Larrea-family companies. The forensic review found that total purchases from parent affiliates grew materially year-over-year — faster than revenue — that the payable balance owed to affiliates expanded sharply, and that purchases from Asarco rose by an order of magnitude. Oversight of all of this rests on the company’s own Audit Committee review framework; no independent fairness opinion or market benchmarking of affiliate pricing is disclosed, several officers and directors are simultaneously officers or directors of Grupo Mexico entities, and the filing’s own risk factors concede that rising parent financial obligations could result in the parent obtaining loans, increased dividends or other funding from the company.

Two adjacent findings reinforce the pattern and are noted here as watch items. First, the Mexican defined-benefit pension plan’s allocation to Grupo Mexico’s own shares increased again year-over-year — a related-party concentration decided by plan fiduciaries that ties the plan’s funded status to the controlling shareholder’s equity, and a governance signal more than a balance-sheet risk given the plan is overfunded. Second, shortly after year-end, the controlled board approved a discretionary, non-contractual “solidarity contribution” to the government of Sonora, Mexico — a payment of meaningful size that was not approved by minority shareholders, benefits the operating jurisdiction of the parent’s broader interests, and is disclosed under commitments rather than subsequent events, where a reader could miss it. Neither item is individually large relative to the company; both illustrate how far the parent’s discretion reaches into company-related pools of capital.

The financial consequence is structural: the small public float bears a pro-rata share of every dollar paid to parent affiliates at prices that cannot be independently verified from the filing, and the cash dividend — raised again in the most recent year — flows overwhelmingly to the parent, consistent with the risk factor’s own warning about parent funding needs. The trigger for materialization is any period of parent balance-sheet stress, which history suggests would be met through the channels the filing itself enumerates.

Probability: High (the structure is in place and the transaction volume is growing; the question is degree, not existence) | Timeframe: Immediate and continuous | Quantified potential impact: Not quantifiable from the filing — which is precisely the problem. The cost to minority holders is the unobservable spread between affiliate pricing and market pricing, applied to a growing volume of related-party purchases.

Peruvian “labor shares” litigation — escalated enforcement orders, unquantified exposure

sources The forensic review flags this as a red-level legal risk, and it deserves prominence because it changed materially during the year. The decades-old Garcia Ataucuri lawsuit over Peruvian labor shares, which was absent from the prior year’s litigation disclosure entirely, re-emerged in the FY2025 filing at the judgment-execution stage: in December 2025 the company learned that a Lima civil court had ordered the physical delivery of millions of investment shares held by the Peruvian Branch and an affiliate to plaintiffs, and had instructed Peru’s securities registry to record ownership in their favor — adopting, before the court-ordered appraisal is final, the plaintiffs’ interpretation that one labor share equals one investment share. The company appealed within days and filed a constitutional protection action; in February 2026 a constitutional court ruled in its favor and enforcement was provisionally suspended. That reversal is first-instance and provisional, appeals are expected to be resolved during 2026, and the company states it cannot predict the outcome. No accrual or estimated exposure is disclosed. §

Two features warrant skepticism toward the “cannot be reasonably estimated” posture. The courts have already specified share quantities — the exposure is not formless. And an adverse final ruling would do more than transfer the named shares: it would set the valuation precedent for the broader class of labor-share claims against the Branch. The fact that this matter went from undisclosed in one annual filing to active enforcement orders in the next is itself a disclosure-cadence concern.

Probability: Medium (the company prevailed at the constitutional stage, but provisionally and at first instance) | Timeframe: Immediate — appellate rulings expected during 2026 | Quantified potential impact: Not quantified by the company; an adverse outcome would transfer economic interests in the Peruvian Branch to plaintiffs and establish a conversion precedent for the wider class, making this a potentially material dilution-of-economics event rather than an ordinary contingency.

Copper price dependence amplified by mark-to-market earnings quality

sources The structural risk is familiar — financial performance depends on copper, molybdenum, zinc and silver prices set by forces outside the company’s control, with Chinese demand singled out and extended price declines capable of triggering inventory writedowns, impairments and curtailment. What is specific to this year is how much of the reported result is itself a price mark. The forensic review flags, at yellow level, that trade receivables grew several times faster than sales, concentrated in the Mexican open-pit segment, driven by provisionally priced copper marked near the year’s record prices; the embedded-derivative receivable from provisional pricing more than doubled, a large open volume of provisionally priced copper settles in the first half of 2026, and the year’s net sales benefited from a positive provisional-pricing adjustment where the prior year’s was negative. The mechanism is standard for the industry and properly disclosed — but it means a meaningful slice of the record year reverses mechanically if copper retraces through the settlement windows. Concentration of year-end receivables in the largest customer also rose.

Two further yellow-flagged items belong in the same earnings-quality frame. The asset-retirement-obligation estimate has now been revised downward two years running — principally at Buenavista, in a jurisdiction where the company itself notes no enacted closure law exists — with the revision credited to cost of goods sold each time; a portion of the reported cost improvement is therefore estimate-driven, not operational. And the auditor’s sole critical audit matter remains the capitalization of leachable material on leach pads, mainly in Mexico — a large, long-dated, judgment-intensive inventory balance whose recoverability rests on copper grade, solubility and recovery-rate assumptions; no adverse indicator surfaced this year, but a downward revision to those assumptions would charge a substantial asset to cost of sales.

Probability: High for the price-mark reversal mechanism operating in some degree (it is mechanical); Medium for a reversal large enough to dent reported results visibly | Timeframe: Immediate — H1 2026 settlement windows | Impact: A copper retracement would simultaneously reverse provisional-pricing gains, deflate the receivable, and compress margins on new sales — the same variable hitting revenue, working capital and earnings quality at once.

Social license and project execution in Peru — the growth plan’s single point of failure

sources The organic growth plan to 2033 runs disproportionately through Peruvian ground that has already proven contestable. Tia Maria — the flagship, targeted for 2027 start-up with heavy capital committed and construction well advanced — now faces a longer list of lawsuits seeking to nullify its environmental approval, its construction license, or the project itself, with new claims filed during the year; the company calls them meritless and cannot estimate the contingency. The forensic review adds a yellow flag: the year’s other-expense line includes an unexplained, unquantified write-off of certain Tia Maria expenses — a soft signal of scope or capitalization revisions in the same year management reports accelerating progress, and one the filing does not explain. The project’s region was the site of violent community opposition within recent memory, as was Cuajone in 2022, where protests blocked the railway and seized water facilities. Los Chancas, the next project in the queue, is currently blocked outright by illegal miners occupying the project area. Taxco in Mexico has been on strike since 2007.

Overlaying all of this is Peruvian political instability of an unusual intensity even by local standards: congressional removal of the president in late 2025, the impeachment of the interim successor within months, a transitional government, and general elections due in April 2026. A meaningful share of net sales and effectively all of the near-term growth pipeline depend on the post-election government’s posture toward large-scale mining, royalties and the rule of law. §

Probability: Medium for material Tia Maria delay or cost escalation; High for continued Los Chancas blockage | Timeframe: 1–2 years (Tia Maria to 2027; elections April 2026) | Impact: Delay converts committed capital into a non-earning asset and pushes out the production growth that justifies the elevated investment program; outright cancellation — the precedent the lawsuits seek — would force a write-down and gut the 2033 volume target.

Mexican fiscal and regulatory tightening — and a filing error on the company’s own tax rate

sources The forensic review identified a red-level contradiction between consecutive filings on the Mexican special mining duty: the prior-year 10-K disclosed an increase in the royalty rate effective January 1, 2025, while the FY2025 filing’s tax footnote describes the 2025 rate at the lower, pre-increase level with no explanation of any repeal — and the filing’s own tax-reconciliation dynamics do not cohere with a single stated rate. This has since been resolved externally against the enacting decree published in Mexico’s Diario Oficial de la Federación on December 19, 2024: the special mining duty in force from January 1, 2025 is 8.5%, the higher rate, and the FY2025 footnote’s reference to 7.5% is incorrect as a description of enacted law. Two implications follow. Substantively, the enacted burden on the Mexican operations is the heavier one — a recurring charge at the higher rate, alongside the doubled extraordinary duty on precious-metals receipts that the filing does disclose correctly. And as a governance observation, a misstatement of the company’s own statutory royalty rate in the audited tax footnote — on a nine-figure annual charge — is a disclosure-quality lapse that should temper the reader’s confidence in the precision of Note-level tax disclosure generally.

The royalty sits within a broader tightening trend: the recent Mining Law amendments shortened concession terms, added water-use conditions, closure and remediation guarantees, and a contribution from new projects’ earnings to indigenous communities — changes now under Supreme Court review, with the company expecting no negative impact, a characterization that is management’s view rather than a settled outcome. A constitutional reform introducing popular election of judges creates effects on the judicial system the company itself says cannot currently be determined, and drug-related violence has disrupted commercial logistics in certain states, so far with limited operational impact. In Peru, new progressive-closure guarantee regulation opens a multi-year window that could raise funding requirements. §

Probability: High that the fiscal direction in both jurisdictions remains tighter; Low–Medium for a further step-change within the forecast horizon | Timeframe: Immediate (the higher royalty is already enacted) to 3–5 years (mining-law litigation, judicial reform) | Impact: The royalty operates as a permanent margin haircut on the Mexican segments — the larger half of the asset base — and the correct, higher rate must flow through any forward tax and cash-flow modeling; the valuation in Sections 4 and 6 uses the verified enacted rate.

2.2 Upside Catalysts

sources The catalyst picture is thinner than the risk picture, and that asymmetry should be stated plainly: five identified risks against three catalysts, of which only one is a discrete, dateable event. The catalysts are real — one is already in the run-rate — but they are operational and macro in nature, not binary re-rating events, and the largest of them (Tia Maria) is simultaneously the locus of the fourth risk above.

Tia Maria commissioning — the first new production unit in years

sources Construction is advancing after a decade of delay: earthworks, access infrastructure, the electrical substation and transmission line are progressing, and management targets operations in 2027. As a low-cost SX-EW cathode operation with desalinated process water, Tia Maria would add copper volume precisely where the existing Peruvian pits are losing it to grade decline — converting the heaviest line in the capital program into earning assets and validating, for the first time since the project’s permitting ordeal began, the company’s ability to deliver a greenfield project in Peru. Successful delivery would also materially de-risk the rest of the Peruvian pipeline in the market’s eyes, since the binding constraint on Los Chancas and Michiquillay is precedent as much as capital. §

Probability: Medium-High for start-up broadly on the 2027 timeline | Timeframe: 1–2 years | Monitoring trigger: Quarterly construction-progress disclosures; resolution of the pending nullification lawsuits; any recurrence of community disruption in Islay province; explanation of the unquantified project write-off in subsequent filings.

The by-product engine — zinc, molybdenum and silver compressing net cash cost

sources This catalyst is already materializing and has room to run. The Buenavista zinc concentrator operated at full capacity in its first complete year, driving zinc output sharply higher; molybdenum and silver production rose across most operations; and the net unit cash cost of copper fell sharply as by-product credits absorbed fixed costs. The structural point is that by-product revenue diversifies the cash-cost position even though it does not diversify commodity exposure: every dollar of by-product credit pushes the company further down the copper cost curve, widening trough-cycle survivability and peak-cycle conversion. Management’s production guidance for the coming year points to continued by-product strength even as copper grades soften.

Probability: High (the assets are built and running) | Timeframe: Immediate and ongoing | Monitoring trigger: Quarterly by-product volumes and the net cash-cost-per-pound trend; zinc and molybdenum prices, which determine how much of the volume gain reaches the credit line.

Copper market deficit and structurally tight inventories

sources Management estimates a copper market deficit for the coming year, with global inventories covering only days of demand, against a demand backdrop structurally supported by electrification and the energy transition — a dynamic the filing itself highlights, alongside rising buyer preference for responsibly certified copper, which the company has pledged to deliver across its entire production. For the lowest-cost producers, a deficit market is the highest-leverage environment available: price strength flows through a cost base that is simultaneously being compressed by the by-product engine. The honest caveat is that this catalyst is entirely outside the company’s control, is already partly reflected in the near-record prices at which the year ended, and is the mirror image of Risk 3 — the same provisional-pricing mechanism that poses reversal risk would extend gains if tightness persists.

Probability: Medium (deficit forecasts are management’s view of a notoriously cyclical market) | Timeframe: Immediate to 1–2 years | Monitoring trigger: Exchange inventory levels; Chinese refined-copper demand indicators; the trajectory of U.S. tariff policy on copper products, which the filing flags as a live volatility channel in both directions.

2.3 Risk & Catalyst Summary

sources | # | Item | Type | Probability | Timeframe | Status | Monitoring Trigger | |—|—|—|—|—|—|—| | 1 | Grupo Mexico related-party economics and controlled-board discretion | Risk | High | Immediate / continuous | Active | Related-party purchase and payable trends in each 10-K; further discretionary payments approved by the board; pension allocation to parent shares | | 2 | Peruvian labor-shares litigation (Garcia Ataucuri enforcement) | Risk | Medium | Immediate (rulings due 2026) | Active | Superior Court and constitutional appeal rulings in Lima during 2026 | | 3 | Copper price reversal amplified by provisional-pricing marks; estimate-driven cost credits | Risk | Medium-High | Immediate (H1 2026 settlements) | Active | Q1–Q2 2026 provisional-pricing settlement effects; receivable balance; any further ARO credits or leach-pad assumption changes | | 4 | Peruvian social license and project execution (Tia Maria, Los Chancas, elections) | Risk | Medium | 1–2 years | Active | Tia Maria lawsuit outcomes and construction milestones; Los Chancas site control; April 2026 election result and mining policy of the incoming government | | 5 | Mexican fiscal and regulatory tightening; royalty-rate disclosure error | Risk | High (enacted) | Immediate to 3–5 years | Active | FY2026 10-K correction of the royalty disclosure; Supreme Court ruling on Mining Law amendments; judicial-reform implementation | | 6 | Tia Maria commissioning toward 2027 start-up | Catalyst | Medium-High | 1–2 years | Monitoring | Construction progress disclosures; legal docket; community relations in Islay | | 7 | By-product engine compressing net cash cost | Catalyst | High | Immediate / ongoing | Active | Quarterly by-product volumes and net cash-cost trend | | 8 | Copper market deficit and tight inventories | Catalyst | Medium | Immediate to 1–2 years | Monitoring | Exchange inventories; Chinese demand; U.S. tariff developments |

2.4 Risk Interdependencies

sources These risks do not sit in separate compartments — they share transmission channels, and the governance risk sits upstream of all of them. A copper price retracement is the single most connective event: it would mechanically reverse the provisional-pricing gains and deflate the receivable (Risk 3), arrive precisely as the capital program peaks into Tia Maria’s final construction phase (Risk 4), and squeeze the cash flow from which both the parent-bound dividend and the affiliate purchases are funded — at which point the filing’s own warning that a stressed parent could extract loans, higher dividends or other funding (Risk 1) stops being theoretical. The Peruvian channel compounds separately: the April 2026 election determines, through one outcome, the judicial and political environment in which the labor-shares appeals are decided (Risk 2), the social-license climate around Tia Maria and Los Chancas (Risk 4), and the durability of the fiscal regime applied to the Peruvian Branch. A populist outcome would not trigger one risk — it would re-price three at once. On the Mexican side, the enacted higher royalty, the Sonora contribution, related-party power pricing and any leach-pad or ARO assumption reversals all land on the same segment income statements, meaning the Mexican open-pit economics could deteriorate through four independent doors simultaneously. The deepest interdependency, however, is structural: because minority shareholders cannot influence the board’s response to any of these events, every risk on this list is borne without the standard mitigant of shareholder pressure. Governance is not the fifth risk — it is the multiplier on the other four.

2.5 ESG & Regulatory Exposure

sources The ESG profile is genuinely two-sided, and both sides are specific to this filing. On the credit side: the company reports a meaningful reduction in lost-time injuries versus the prior year, running well below the comparable U.S. industry benchmark; its open-pit mines in both countries hold The Copper Mark accreditation including compliance with the ICMM Global Industry Standard on Tailings Management, with a new internal tailings-review committee; clean-energy certificates indicate the Peruvian operations’ electricity was fully renewable, meeting the company’s target ahead of schedule; sustainability ratings improved, including continued index inclusion; and the company has pledged certification of its entire copper production under international responsible-sourcing standards — directly relevant given the filing’s observation that buyers increasingly demand responsibly sourced copper. The social architecture around Tia Maria — education, healthcare, supplier development, large-scale infrastructure through Peru’s Works for Taxes mechanism, a grievance mechanism at all sites and a UN-guided human rights due diligence process — is the company’s explicit answer to its most expensive historical ESG failure: lost years of project delay.

On the debit side, the same filing records workforce fatalities during the year; a tailings-dam risk disclosure that is candid about catastrophic potential; a legacy environmental docket including dozens of pending civil, collective and constitutional actions from the 2014 Buenavista spill (all characterized by the company as without merit and immaterial in aggregate — its view, not a settled outcome); the Guaymas terminal acid-spill matter approaching restart; and the unresolved Taxco strike, now old enough that it functions as a standing illustration of labor-relations failure at one unit even as Peru’s long-term no-stoppage agreements demonstrate the opposite. Two ESG items also loop back into governance: the renewable power earning the company its climate progress is purchased from Grupo Mexico affiliates under long-dated contracts whose pricing is not independently benchmarked, and the Sonora “solidarity contribution” blurs the line between community investment and parent-aligned political spending.

The regulatory exposure map is concentrated and live: the enacted higher Mexican mining royalty (with the filing’s own erroneous disclosure of it); the Mining Law amendments under Supreme Court review; Mexican judicial reform with effects the company says cannot be determined; Peru’s progressive-closure guarantee regulation opening a funding-requirement window; the April 2026 Peruvian elections; and U.S. tariff policy on copper products, which the filing links directly to volatility in both its product prices and its stock. None of these is generic sector backdrop — each attaches to a specific disclosure in this 10-K, and each carries a date or docket on which it can be monitored.

Section 3 — Financial Analysis & Historical Performance

sources

Three-Statement Linkage Confirmation: - Net Income ties (Income Statement → Cash Flow Statement): confirmed via the recalculated workbook. Net income throughout this section is income attributable to Southern Copper Corporation (i.e., net of the non-controlling interest in subsidiaries), consistent with the figure that opens the consolidated cash flow statement reconciliation. - Cash ties (Balance Sheet → Cash Flow Statement): confirmed via the recalculated workbook — year-end cash and equivalents on the balance sheet agree with the ending cash position of the cash flow statement in each year presented. - Retained Earnings reconciliation (Beg RE + NI − Dividends = End RE): confirmed via the recalculated workbook, noting that distributions include both cash dividends and the stock dividends paid from treasury shares beginning in 2024, both of which are charged against retained earnings. This is why retained earnings decline across the period even as the company earns record profits — a capital-return artifact, not an operating one, and it is analyzed in 3.2B.

3.1A Income Statement

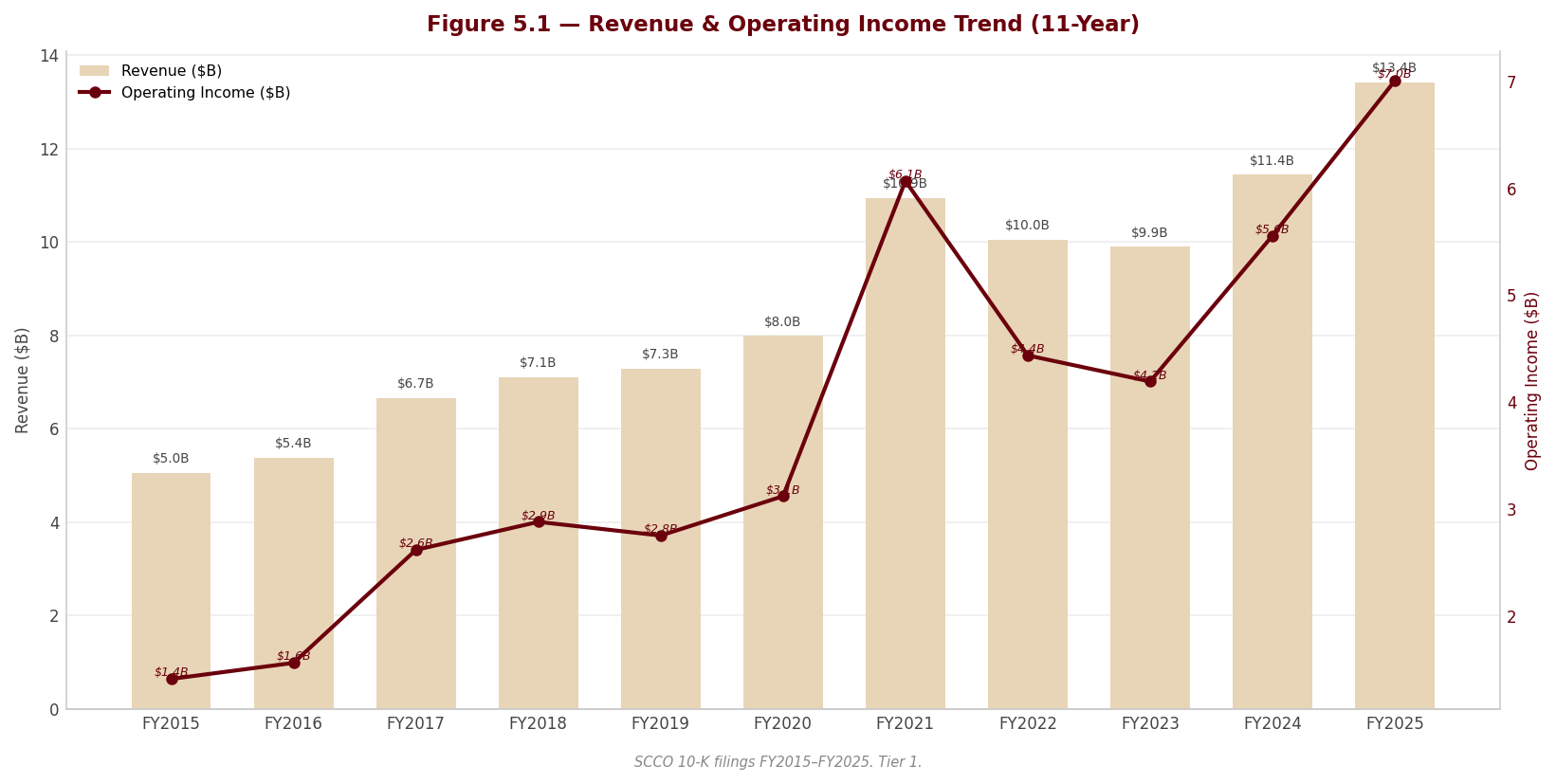

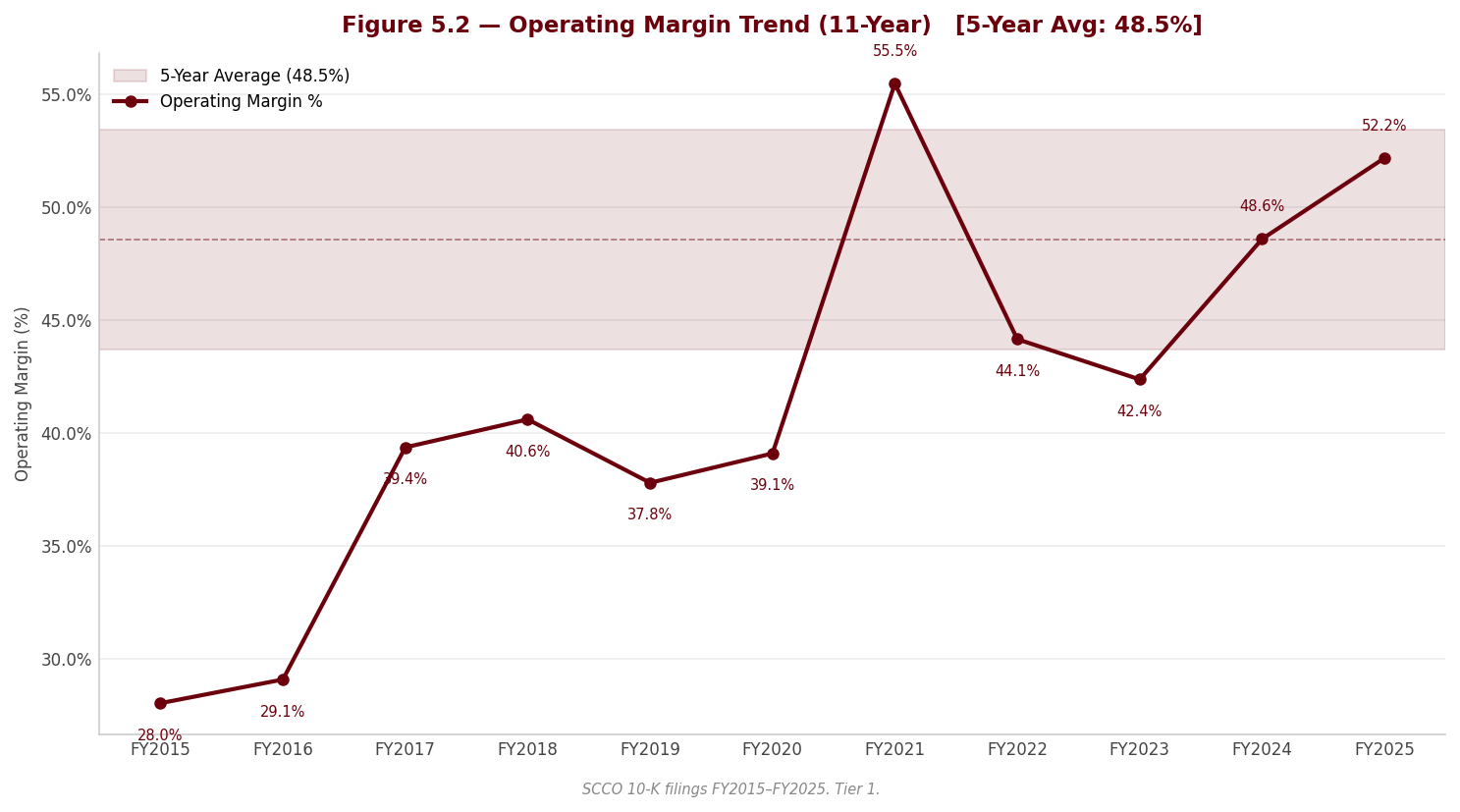

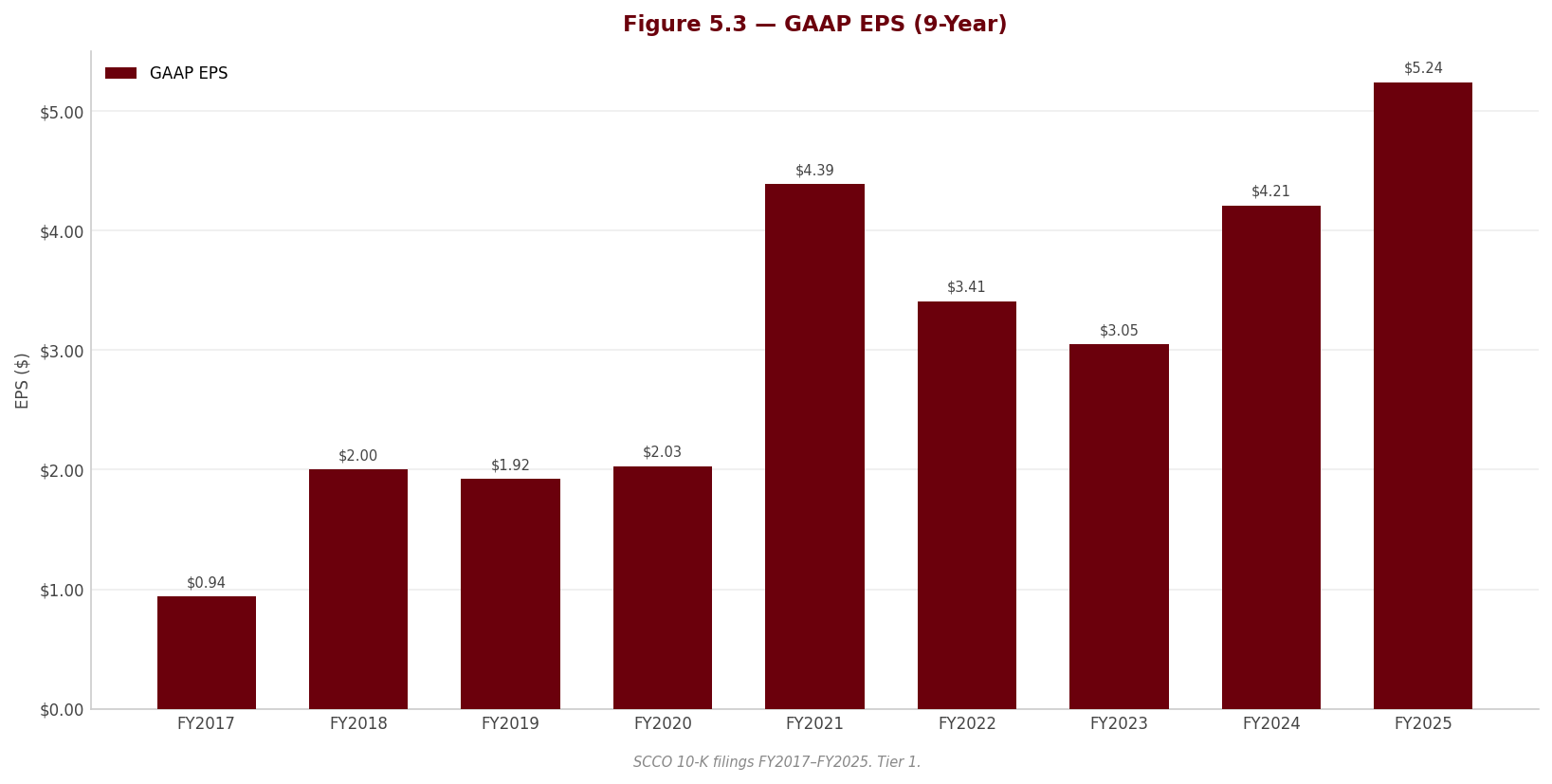

sources | | FY2021 | FY2022 | FY2023 | FY2024 | FY2025 | |—|—|—|—|—|—| | Revenue ($M) | 10,934.1M | 10,047.9M | 9,895.8M | 11,433.4M | 13,420.0M | | YoY Growth | 36.9% | -8.1% | -1.5% | 15.5% | 17.4% | | Cost of Goods Sold ($M) | 3,894.4M | 4,649.1M | 4,687.7M | 4,841.4M | 5,359.2M | | Gross Profit ($M) | 7,039.7M | 5,398.8M | 5,208.1M | 6,592.0M | 8,060.8M | | Gross Margin | 64.4% | 53.7% | 52.6% | 57.7% | 60.1% | | D&A ($M) | 806.0M | 796.3M | 833.6M | 845.9M | 868.4M | | EBITDA ($M) | 6,871.1M | 5,232.1M | 5,025.9M | 6,400.6M | 7,870.1M | | EBITDA Margin | 62.8% | 52.1% | 50.8% | 56.0% | 58.6% | | EBITDA Growth | 76.4% | -23.9% | -3.9% | 27.4% | 23.0% | | EBIT ($M) | 6,065.1M | 4,435.8M | 4,192.3M | 5,554.7M | 7,001.7M | | EBIT Margin | 55.5% | 44.1% | 42.4% | 48.6% | 52.2% | | Interest Expense ($M) | 387.9M | 387.1M | 376.3M | 376.5M | 416.7M | | Pre-Tax Income ($M) | 5,696.8M | 4,247.8M | 3,955.8M | 5,357.4M | 6,784.3M | | Tax Expense ($M) | 2,299.2M | 1,596.1M | 1,518.9M | 1,975.3M | 2,470.1M | | Effective Tax Rate | 40.4% | 37.6% | 38.4% | 36.9% | 36.4% | | Net Income ($M) | 3,397.1M | 2,638.5M | 2,425.2M | 3,376.8M | 4,334.9M | | Net Margin | 31.1% | 26.3% | 24.5% | 29.5% | 32.3% | | Net Income Growth | 116.4% | -22.3% | -8.1% | 39.2% | 28.4% | | Diluted EPS | $4.39 | $3.41 | $3.05 | $4.21 | $5.24 | | EPS Growth | 116.3% | -22.3% | -10.6% | 38.0% | 24.5% | | Diluted Shares (M) | 773 | 773 | 795 | 803 | 827 |

Source: Southern Copper Corporation Form 10-K filings, consolidated statements of operations, FY2021–FY2025, as compiled in the verified workbook. Net income is attributable to Southern Copper Corporation. Per-share basis note: FY2023–FY2025 per-share figures and share counts are retroactively adjusted for the stock dividends paid since 2024, per the FY2025 10-K; FY2021–FY2022 figures are as printed in the original filings on a pre-stock-dividend basis and are not directly comparable with FY2023–FY2025. EPS growth rates and any EPS or share-count CAGR spanning the FY2022→FY2023 boundary therefore mix the two bases.

CAGR Summary

| Metric | 3Y CAGR | 5Y CAGR | 10Y CAGR |

|---|---|---|---|

| Revenue | 10.1% | 10.9% | 10.3% |

| EBITDA | 14.6% | 15.1% | 15.1% |

| Net Income | 18.0% | 22.5% | 19.4% |

| Diluted EPS | 15.4% | 20.9% | — |

| FCF | 22.7% | 9.3% | — |

Source: verified workbook (SCCO_Portfolio.xlsx), figures traceable via lineage.json to the cited filings.

3.1B Income Statement — Analysis

sources The revenue story is a price story with a volume kicker — and the volume is not copper. The five-year arc traces a full commodity cycle: the FY2021 copper price surge produced 36.9% growth to 10,934.1M, the FY2022–FY2023 retracement took revenue down -8.1% and then -1.5% to a trough of 9,895.8M, and the recovery delivered record net sales of 11,433.4M and then 13,420.0M. The composition of the FY2025 record matters more than its size. Management attributes it to higher sales volumes of molybdenum, zinc and silver, higher prices for copper, silver, molybdenum and zinc, and upward adjustments on provisionally priced sales — while copper mine production itself declined modestly on lower ore grades at Toquepala, Cuajone and Buenavista, where the new concentrator was dedicated to zinc. In other words, the record year rests on price and by-product volume, not copper volume. That distinction is structurally important: the by-product volume gain (principally the Buenavista zinc concentrator running at full capacity in its first complete year) is durable and compounds, whereas the price component — including the provisional-pricing mark discussed below — reverses with the commodity cycle. The 10.9% five-year revenue CAGR should accordingly be read as a cycle-amplified figure measured trough-to-peak, not a sustainable organic growth rate.

Margins are recovering toward — but have not regained — the FY2021 cycle peak, and not all of the recovery is operational. Gross margin traced the cycle from 64.4% at the FY2021 peak down to 52.6% at the trough and back to 60.1%, with EBITDA margin following the same path from 62.8% to 50.8% to 58.6%. The mechanism is classic mining operating leverage: cost of sales grew from 3,894.4M to 5,359.2M across the period — a steady grind higher through both halves of the cycle, driven by workers’ participation (profit-linked, so partly self-correcting), purchased copper, repair materials, energy and exchange-rate effects — while revenue swung far more violently around it. The margin recovery since FY2023 is therefore predominantly a revenue-side, cyclical phenomenon, with one genuine structural assist: by-product revenue from zinc, molybdenum and silver, which cut the net unit cash cost of copper sharply and pushes the company further down the industry cost curve. Two cautions temper the headline margin, both from the forensic review and developed under Quality of Earnings below: recurring asset-retirement-obligation estimate credits flattered cost of sales in both FY2024 and FY2025, and part of the FY2025 revenue line is a mark-to-market on unsettled copper.

Major Movers

-

Metal prices and the provisional-pricing swing — cyclical, and partly unsettled. The single largest driver of the 17.4% top-line gain was price, and within it the swing on provisionally priced sales: FY2025 net sales include a positive provisional-pricing adjustment where the prior year’s was negative, with copper marked near the year’s record price on volumes settling January–June 2026. This is standard industry mechanics, properly disclosed — but it means a slice of the record revenue and the associated receivable is a price mark, not settled cash, and it reverses mechanically if copper retraces through the settlement windows. Historically this is exactly the pattern of FY2021→FY2022, when revenue fell -8.1% as the price peak unwound.

-

The Buenavista zinc concentrator and the by-product engine — structural. Zinc production rose sharply on the concentrator’s first full year at capacity, and molybdenum and silver output increased across most operations. This is the one component of the FY2025 record that does not depend on the copper price: it adds volume, diversifies the revenue mix, and — through by-product credits — drove the sharp fall in net unit cash cost even as the gross cash cost per pound rose slightly on lower copper production. It is the principal reason EBITDA of 7,870.1M now exceeds the FY2021 cycle-peak level of 6,871.1M despite lower copper output.

-

Cost-of-sales inflation, including a growing related-party component — partly structural. COGS rose from 4,841.4M to 5,359.2M, led by workers’ participation, purchased copper, repair materials, sales expenses, exchange-rate effects and energy. The forensic review flags, at red level, that a material and growing share of this cost base flows to Grupo Mexico affiliates — captive power for the Mexican operations under long-dated contracts with parent-owned generators, rail freight, construction, services, and metal purchases from sister company Asarco that rose by an order of magnitude — with affiliate purchases growing faster than revenue and no independent benchmarking of pricing disclosed. For the income statement, the implication is that a portion of the cost structure is priced inside the controlled group and is unverifiable as arm’s-length from the filing; minority holders bear it pro-rata.

-

ARO estimate credits to cost of sales — non-operational and recurring in the same direction. The forensic review flags, at yellow level, that updates to Mexican mine-closure estimates (mainly the Buenavista life-of-mine update) produced a credit to cost of goods sold in FY2025, following a similar and slightly larger credit in FY2024, with a further small Peruvian credit in late 2025 — in a jurisdiction where, by the company’s own disclosure, no enacted law requires closure, so the obligation rests heavily on management estimates. A change in estimate that recurs in the same direction, two years running, at the same unit, argues for treating a portion of the reported cost improvement as accounting rather than operations when extrapolating the margin trend.

-

The tax line — structurally heavy, and with an unresolved disclosure contradiction. The effective tax rate has sat far above the U.S. federal statutory rate throughout the period (40.4% at the FY2021 peak, 36.4% in FY2025), driven by Peruvian and Mexican rate differentials, mining royalties, the special mining tax and non-deductible interest. The forensic review (yellow) is explicit that this burden is structural, not transient: the U.S. foreign-tax-credit carryforward carries a full valuation allowance that grew again in 2025, with management itself stating the excess credits are unlikely ever to be used — so double taxation is not relieved in practice and the full blended rate is the right modeling input. Compounding this, the forensic review identified a red-level contradiction between consecutive filings on the Mexican mining royalty rate — the FY2025 tax footnote describes a 2025 rate below the increase the FY2024 filing disclosed as enacted, with no explanation, and the filing’s internal tax-reconciliation dynamics do not cohere with a single stated rate. As established in Section 2, external verification against the enacting decree resolves the contradiction in favor of the higher rate; the point for this section is that a misstatement of the company’s own statutory royalty rate, in the audited tax footnote, on a nine-figure recurring charge, is a disclosure-quality lapse that should temper confidence in Note-level tax precision generally.

Quality of earnings. Beyond the ARO credits and the provisional-pricing mark already covered, three further items condition the FY2025 result. First, non-operating results deteriorated on a swing in other income that included an unquantified write-off of certain Tia Maria project expenses (versus an insurance recovery the prior year) — flagged by the forensic review as a soft signal of scope or capitalization revisions the filing does not explain — plus higher interest expense following Minera Mexico’s February 2025 note issuance (interest expense rose from 376.5M to 416.7M), partially offset by higher interest income on the enlarged cash balance. Second, the auditor’s sole critical audit matter remains the capitalization of leachable material on Mexican leach pads — a large, judgment-intensive balance whose recoverability rests on grade, solubility and recovery assumptions; no adverse indicator surfaced this year, but a downward revision would charge a substantial asset to cost of sales. Third, on a per-share basis, the record is diluted in transit: stock dividends paid from treasury shares have grown the diluted count from 795M to 827M in two years, so EPS of $5.24 grew 24.5% against net income growth of 28.4% — a roughly four-point annual drag that is policy-driven and ongoing.

⚠ Items to Watch. If gross margin falls back below the 52.6% trough level, the cyclical margin recovery has fully reversed and the by-product cost cushion has been overwhelmed — trough-cycle earnings assumptions would need rebasing. If the effective tax rate rises above the 40.4% FY2021 level, the Mexican royalty escalation is biting harder than the structural mid-30s base and forward FCF modeling must be re-cut. If FY2026 interim filings show a negative provisional-pricing adjustment, quantify it against the 17.4% FY2025 growth print before annualizing any revenue trend. And EPS growth persistently lagging net income growth by more than the current gap (compare 24.5% vs 28.4%) would indicate the stock-dividend dilution is accelerating as treasury shares deplete.

3.2A Balance Sheet

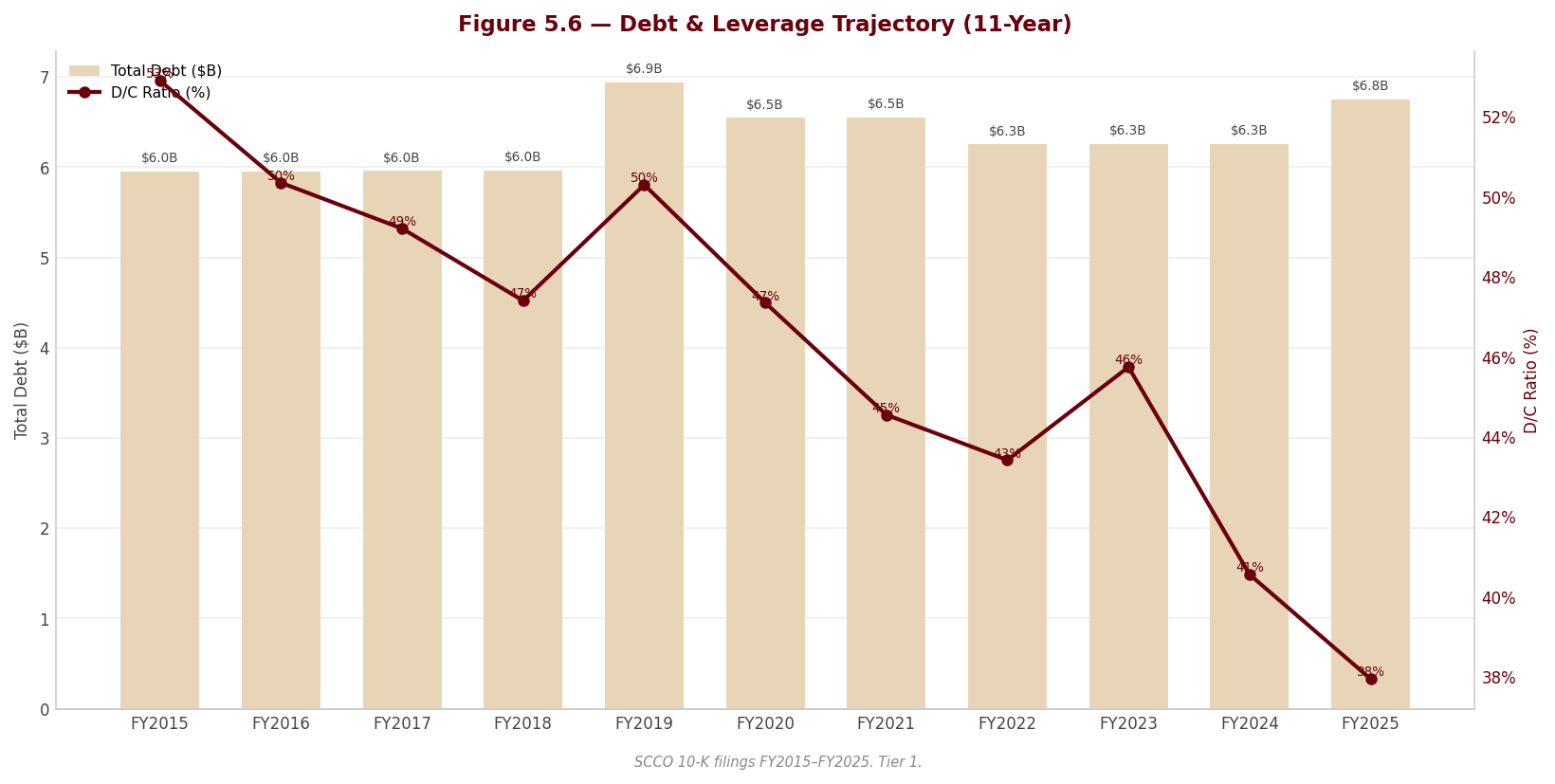

sources | | FY2021 | FY2022 | FY2023 | FY2024 | FY2025 | |—|—|—|—|—|—| | ASSETS | | | | | | | Cash & Equivalents ($M) | 3,002.0M | 2,069.7M | 1,151.5M | 3,258.1M | 4,304.6M | | Receivables ($M) | 1,358.7M | 1,394.1M | 1,141.1M | 1,189.6M | 1,951.2M | | Inventory ($M) | 972.9M | 1,014.0M | 1,016.9M | 1,048.9M | 1,058.1M | | Total Current Assets ($M) | 6,139.6M | 5,188.0M | 4,429.5M | 6,174.3M | 8,352.5M | | PP&E, net ($M) | 9,464.4M | 9,597.0M | 9,782.9M | 9,883.3M | 10,272.2M | | Goodwill & Intangibles ($M) | 138.1M | 135.0M | 130.2M | 124.6M | 122.4M | | Total Assets ($M) | 18,297.6M | 17,277.0M | 16,725.3M | 18,713.5M | 21,381.4M | | LIABILITIES & EQUITY | | | | | | | Short-term Debt ($M) | 299.7M | 0.0M | 0.0M | 499.8M | 0.0M | | Total Current Liabilities ($M) | 2,250.0M | 1,236.0M | 1,388.5M | 2,248.1M | 2,145.1M | | Long-term Debt ($M) | 6,247.9M | 6,251.0M | 6,254.6M | 5,758.5M | 6,750.7M | | Total Debt ($M) | 6,547.6M | 6,251.0M | 6,254.6M | 6,258.3M | 6,750.7M | | Net Debt ($M) | 3,545.6M | 4,181.3M | 5,103.1M | 3,000.2M | 2,446.1M | | Total Liabilities ($M) | 10,089.8M | 9,130.8M | 9,244.1M | 9,475.3M | 10,276.5M | | Shareholders’ Equity ($M) | 8,149.2M | 8,084.2M | 7,418.1M | 9,171.6M | 11,038.1M | | Retained Earnings ($M) | 7,769.7M | 7,702.0M | 7,033.5M | 6,839.6M | 5,797.2M | | Key Ratios | | | | | | | Current Ratio | 2.7x | 4.2x | 3.2x | 2.7x | 3.9x | | Net Debt / EBITDA | 0.5x | 0.8x | 1.0x | 0.5x | 0.3x | | Debt / Equity | 0.8x | 0.8x | 0.8x | 0.7x | 0.6x | | Book Value / Share | $10.54 | $10.46 | $9.33 | $11.42 | $13.35 |

Source: Southern Copper Corporation Form 10-K filings, consolidated balance sheets, FY2021–FY2025, as compiled in the verified workbook. Short-term debt of zero in FY2023 and FY2025 reflects the balance sheet as printed — no current portion of long-term debt was outstanding at those year-ends.

3.2B Balance Sheet — Analysis

sources Asset composition: a capital-intensive organic story, with one judgment-heavy balance inside it. This is a miner’s balance sheet built by drilling, not dealmaking: PP&E of 10,272.2M is the largest asset, goodwill and intangibles are immaterial at 122.4M and shrinking, and the asset base has grown from 16,725.3M to 21,381.4M over two years almost entirely through retained cash and capital projects. The most consequential change is liquidity: cash and equivalents rebuilt from a trough of 1,151.5M to 4,304.6M — a deliberate war chest, since the company carries no committed revolver and management explicitly rests its liquidity plan on cash on hand and internally generated funds. One asset deserves standing scrutiny: the long-term ore-stockpiles-on-leach-pads balance, the auditor’s sole critical audit matter for a second consecutive year, whose carrying value depends on copper grade, solubility-index and recovery-rate estimates. In 2025 consumption slightly exceeded additions, so the balance edged down — no adverse signal, but it remains the single highest-judgment account on this balance sheet and a multi-hundred-million-dollar charge to cost of sales if recovery assumptions are cut.

Leverage: gross debt static, net leverage melting, structure clean — with one typographical caveat. Total debt has been essentially flat for five years (6,547.6M to 6,750.7M); the deleveraging is entirely a cash phenomenon, with net debt falling from a 5,103.1M peak to 2,446.1M and Net Debt/EBITDA from 1.0x to 0.3x. The forensic review’s structural assessment is favorable: all debt is USD fixed-rate, the April 2025 maturity was repaid and only a small Yankee bond tranche matures within five years, the single disclosed financial maintenance covenant was met with very wide headroom, the new Minera Mexico 2032 notes are rated investment grade by all three agencies, and no cross-defaults, restricted cash or borrowing-base facilities are disclosed. Refinancing and covenant risk is minimal at current profitability — the trade-off, again, is that with no revolver, liquidity is the cash balance. One disclosure-quality note from the forensic review: the filing states two different coupons for the new 2032 notes in the debt table versus the narrative — a typographical error inside the filing that the verified workbook resolves in favor of the narrative rate, but a second instance (after the royalty-rate contradiction) of imprecision in audited note disclosure. This trajectory is consistent with management’s stated priority of a prudent capital structure; the question raised in Section 2 — whether the growing cash pile is also an attractive resource for a controlling parent with funding needs — is a governance question, not a credit one.

Working capital: the receivables build is the flag, and it is a price mark, not a collection problem. Receivables jumped from 1,189.6M to 1,951.2M — growth several times the 17.4% revenue growth rate — concentrated in the Mexican open-pit segment, and the forensic review (yellow) traces it to provisionally priced copper marked near the year’s record price, with the embedded-derivative receivable more than doubling and the largest customer’s share of year-end receivables rising markedly. DSO accordingly stretched from 37 days to 43 days. The right reading is earnings-quality, not credit-quality: if copper retraces through the H1 2026 settlement windows, the receivable deflates and the associated revenue reverses. Outside this item, working capital discipline is genuinely improving — the cash conversion cycle has tightened from 75 days in FY2021 to 64 days, inventory is essentially flat at 1,058.1M against a much larger revenue base, and the current ratio of 3.9x is ample. Separately, note the optics of retained earnings falling from 7,769.7M to 5,797.2M across five record-profit years: this is the arithmetic of cash dividends plus stock dividends charged against retained earnings, not accumulated losses — but it does mean the equity base is being rebuilt through paid-in capital mechanics rather than retention, and at the current distribution pace the treasury-share pool funding stock dividends depletes within a few years.

⚠ Items to Watch. If Net Debt/EBITDA returns above the 1.0x FY2023 peak, the deleveraging narrative has reversed — most plausibly through a copper downturn coinciding with the enlarged capital program — and the absence of a committed revolver becomes a live constraint rather than a footnote. If DSO holds above the FY2022 level of 50 days after the H1 2026 provisional-pricing settlements wash through, the receivables build is no longer explainable by price marks and demands customer-credit scrutiny, particularly given the rising single-customer concentration. And if cash falls back toward the 1,151.5M FY2023 trough while the dividend is maintained, the liquidity buffer that substitutes for a revolver is being spent.

3.3A Cash Flow Statement

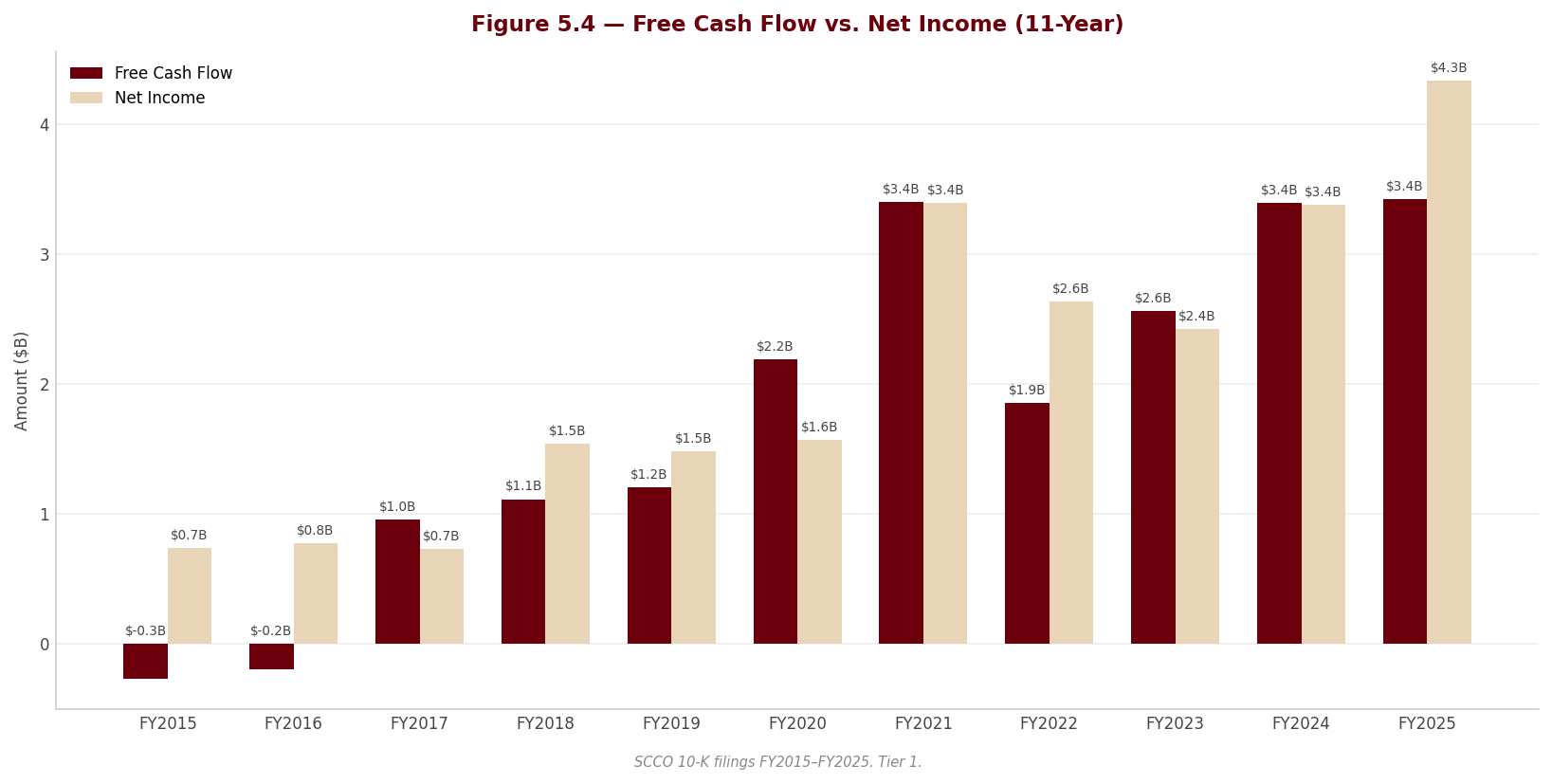

sources | | FY2021 | FY2022 | FY2023 | FY2024 | FY2025 | |—|—|—|—|—|—| | Cash from Operations ($M) | 4,292.4M | 2,802.5M | 3,573.1M | 4,421.7M | 4,752.1M | | Capital Expenditures ($M) | -892.3M | -948.5M | -1,008.6M | -1,027.3M | -1,325.3M | | Free Cash Flow ($M) | 3,400.1M | 1,854.0M | 2,564.5M | 3,394.4M | 3,426.8M | | FCF Margin | 31.1% | 18.5% | 25.9% | 29.7% | 25.5% | | FCF / Share | $4.40 | $2.40 | $3.22 | $4.23 | $4.15 | | FCF Conversion (FCF/NI) | 100.1% | 70.3% | 105.7% | 100.5% | 79.1% | | CapEx / Revenue | 8.2% | 9.4% | 10.2% | 9.0% | 9.9% | | CapEx / D&A | 1.1x | 1.2x | 1.2x | 1.2x | 1.5x | | Dividends Paid ($M) | -2,473.8M | -2,705.8M | -3,092.4M | -1,637.2M | -2,485.1M | | Share Repurchases ($M) | — | — | — | — | — |

Source: Southern Copper Corporation Form 10-K filings, consolidated statements of cash flows, FY2021–FY2025, as compiled in the verified workbook. The share repurchase program has registered no activity since 2016; quarterly stock dividends paid from treasury shares since 2024 are a non-cash distribution and do not appear in this table.

3.3B Cash Flow — Analysis

sources Operating cash flow is genuinely strong, but FY2025 conversion tells you where the earnings quality sits. Cash from operations reached a record 4,752.1M, capping a recovery from the 2,802.5M FY2022 trough, and across the five years FCF conversion has averaged near or above 100% — the signature of a low-cost producer with real cash earnings. The FY2025 wrinkle is instructive: conversion fell to 79.1% from 100.5% even as net income rose 28.4%. The cash went two places, and both are identifiable. First, the working-capital drag from the provisionally priced receivables build documented in 3.2B — earnings recognized at marked prices that have not yet settled into cash; if copper holds, the cash arrives in H1 2026, and if it doesn’t, the earnings partially reverse. Second, the deliberate step-up in capital spending. Neither is a red flag in isolation; together they mean FY2025’s record net income overstates FY2025’s spendable cash by a wider margin than in the prior two years.

CapEx: the harvest period is over. Capital expenditure rose from -1,027.3M to -1,325.3M, taking CapEx/D&A from 1.2x to 1.5x — comfortably in growth-investment territory and the highest of the five years. The filing identifies where it went: the new tailings deposit and concentrator at Buenavista, IMMSA mine development, and the ramp-up of Tia Maria and Los Chancas spending in Peru, with the Board approving a substantially larger program for the coming year centered on Tia Maria and El Pilar. The filing does not split maintenance from growth CapEx, but the trajectory and project list make the inference safe: the company is funding the 2033 volume plan, and investment intensity (CapEx/Revenue of 9.9%) will rise before it falls. The asterisk, per the forensic review, is the unquantified write-off of certain Tia Maria expenses in the same year management reports roughly a quarter of construction complete — unexplained in the filing, and worth a direct question to management, because capitalization discipline on the flagship project is precisely what the enlarged budget will test.

Capital allocation: a dividend machine with no second gear. Over the five years, cash dividends — -2,473.8M, -2,705.8M, -3,092.4M, -1,637.2M, -2,485.1M — absorbed the large majority of cumulative free cash flow, with payout ratios swinging from 48.5% at the FY2024 low to above-earnings levels of 102.6% and 127.5% in the trough years, when the company paid out more than it earned and ran down cash to do it. Buybacks are nonexistent — dormant since 2016, with the remaining authorization covering a trivial number of shares at the current price — and since 2024 the company has layered quarterly stock dividends on top, growing the share count rather than shrinking it. Whether this mix fits the opportunity set is the central capital-allocation question: a company guiding to substantially higher copper volume by 2033, with an enlarged capital program, is simultaneously distributing most of its free cash — and, as the forensic review (red) underscores, the overwhelming share of every cash dividend flows to Grupo Mexico, holder of a super-majority of the stock, consistent with the filing’s own risk-factor language about parent funding needs. The same lens applies to the post-year-end item flagged at yellow: a Board-approved voluntary contribution of meaningful size to government programs in Sonora, Mexico — discretionary, not approved by minority holders, disclosed under commitments rather than subsequent events, and a direct FY2026 claim on cash that benefits the controlling group’s broader operating relationships. The distribution policy, in short, is set by and for the parent; minority holders ride along.

⚠ Items to Watch. If FCF conversion stays below the 70.3% FY2022 trough level for a second consecutive year, cash generation is structurally lagging reported earnings rather than timing-lagging them, and the dividend is being funded from the balance sheet. If the payout ratio returns above the 127.5% FY2023 level while the enlarged capital program is running, something must give — the dividend, the program, or the cash buffer. And if CapEx/Revenue rises materially beyond 9.9% without commensurate Tia Maria progress disclosure, capital intensity is escalating faster than project delivery.

3.4 Returns Analysis

sources | | FY2021 | FY2022 | FY2023 | FY2024 | FY2025 | |—|—|—|—|—|—| | ROIC | 31.1% | 23.1% | 20.8% | 28.4% | 34.7% | | ROE | 44.2% | 32.5% | 31.3% | 40.7% | 42.9% | | ROA | 19.3% | 14.8% | 14.3% | 19.1% | 21.6% | | Interest Coverage | 15.6x | 11.5x | 11.1x | 14.8x | 16.8x |

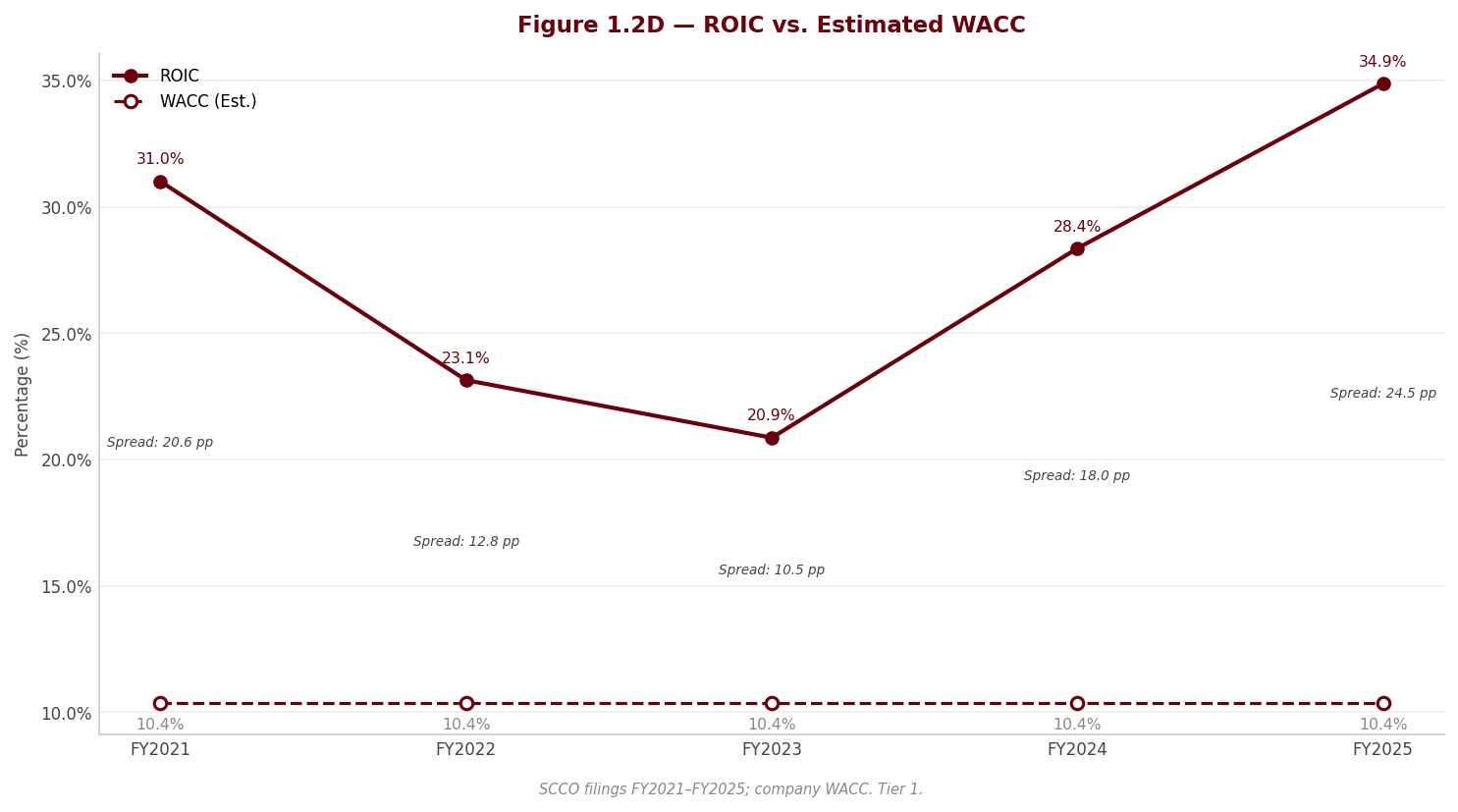

ROIC is the headline finding of this section: at 34.7%, returns on invested capital sit far above any plausible cost of capital for a Latin American miner — the WACC derived in Section 4 will quantify the spread, but no defensible discount rate approaches this level — and critically, even the FY2023 cyclical trough of 20.8% would clear the hurdle comfortably. That trough reading is the more analytically important number: it says the value-creation spread survives the bottom of the copper cycle, which is the direct financial expression of the bottom-quartile cost position described in Section 1. The driver of the spread is the by-product-subsidized cash cost — the company earns a structurally wide gross margin on a price it does not set — and the FY2023→FY2025 expansion from 20.8% to 34.7% is mostly the copper price plus the zinc concentrator, on an invested-capital base that grew only modestly. Two qualifications carry over from earlier subsections: the FY2025 numerator includes the provisional-pricing mark and ARO credits discussed in 3.1B, so the true run-rate ROIC is somewhat below the printed peak; and the enlarged capital program will grow the denominator ahead of the revenue it generates, mechanically compressing ROIC through 2027 even in a flat price environment — a timing effect, not an impairment of the franchise, provided Tia Maria delivers.

The DuPont decomposition shows ROE of 42.9% built as net margin of 32.3% × asset turnover of 0.67x × an equity multiplier of 1.98x. The structure is unambiguous: margin is both the level driver and the swing factor. Asset turnover is low and stable — the physics of a capital-intensive miner, ranging only between 0.56x and 0.67x across the cycle — and the equity multiplier has declined from 2.29x to 1.98x as cash built and equity grew, meaning leverage is subtracting from, not propping up, the ROE trend. An ROE of this magnitude achieved with falling leverage and flat turnover is entirely a margin phenomenon — which is to say, entirely a commodity-price-times-cost-position phenomenon. The practical read-through: model ROE off the copper price deck and the cash-cost curve; the other two DuPont legs are near-constants. Interest coverage of 16.8x — against a fixed-rate, long-dated debt stack — confirms that the capital structure is nowhere near constraining returns.

Source: verified workbook (SCCO_Portfolio.xlsx), figures traceable via lineage.json to the cited filings.

3.5 Altman Z-Score (Most Recent FY)

sources | Component | FY2023 | FY2024 | FY2025 | |—|—|—|—| | X1 (Working Capital / Total Assets) | 0.182 | 0.210 | 0.290 | | X2 (Retained Earnings / Total Assets) | 0.421 | 0.365 | 0.271 | | X3 (EBIT / Total Assets) | 0.251 | 0.297 | 0.327 | | X4 (Equity / Total Liabilities) | 0.802 | 0.968 | 1.074 | | X5 (Revenue / Total Assets) | 0.592 | 0.611 | 0.628 | | Z-Score | 2.71 | 2.93 | 3.08 | | Zone | Gray | Gray | Safe |

The Z-Score of 3.08 crosses back into the safe zone in FY2025 after two years in the upper gray zone (2.71 in FY2023, 2.93 in FY2024), and the trend is moving decisively away from the boundary. The component detail matters more than the headline, because the gray-zone readings were never a distress signal: the soft component throughout is X2 (retained earnings to assets), which is falling — 0.421 to 0.271 — purely because the dividend and stock-dividend policy charges distributions against retained earnings faster than income replenishes them, the capital-return artifact established in 3.2B. Every operating and solvency component is strengthening: X1 (liquidity) rose to 0.290 on the cash build, X3 (asset profitability) to 0.327, and X4 (equity cushion) to 1.074. Read alongside the fixed-rate post-2030 maturity wall, the wide covenant headroom and 16.8x interest coverage, the credit picture is unambiguous: bankruptcy-model risk is not a live concern for this issuer, and the FY2023–FY2024 gray readings were the model penalizing a distribution policy, not detecting fragility. The honest caveat runs the other way — the Z-Score is calibrated to manufacturers and reads a commodity producer’s peak-cycle X3 at face value, so the score will fall mechanically in the next copper downturn; the durable credit anchors are the debt structure and trough-cycle cash generation, not this year’s Z.

Section 4 — Valuation Methodology

sources

4.1 Cost of Capital (WACC)

sources All inputs to the WACC are verified market data (from market-researcher output) or approved assumptions. Computed metrics are marked accordingly.

4.1.1 Cost of Equity

sources | Component | Value | Source | |—|—|—| | Risk-Free Rate (10Y UST) | 4.47% | US Treasury daily yield curve, dual-verified vs. Fed H.15 | | Equity Risk Premium | 4.18% | Damodaran implied ERP (US, trailing, adjusted payout) | | Beta (Levered) | 1.11 | 5-year monthly regression, cross-checked across four sources; used raw, not relevered | | Size Premium | 0.00% | Not applied — mega-cap issuer | | Company-Specific Risk Premium | 2.25% | Damodaran country risk premium dataset (January 2026), Peru/Mexico revenue-weighted | | Cost of Equity (Ke) | 11.61% | CAPM: Rf + β × (ERP + CRP) |

At 11.61%, the cost of equity is demanding for a mega-cap natural-resources issuer — comfortably above what a US-domiciled industrial of comparable scale would carry — and that is by design. With effectively no leverage in the capital structure, the dominant driver of Ke is the premium stack itself: a beta of 1.11 applied to the sum of the equity risk premium and the country risk premium. Beta is used raw rather than relevered. The capital structure has been stable across the past four fiscal years — total debt moved only marginally, with the February 2025 note issuance largely offset by the April 2025 repayment of maturing notes — and at market values the debt-to-equity ratio is trivial, so relevering would alter beta by an amount with no effect on the result.

The country risk premium of 2.25% is not a discretionary add-on. It is taken from the Damodaran country risk premium dataset published in January 2026 and weighted by the company’s revenue split between its two operating geographies, Peru and Mexico, with Peru carrying the larger weight. Every dollar of Southern Copper’s cash flow is generated in these two jurisdictions; pricing the equity off a US-only premium would understate the political, fiscal and social-license risk that the company’s own disclosures document at length (Section 2). One deliberate methodological choice deserves note: the qualitative governance and litigation findings from the forensic review are carried in conviction and in the scenario framing, not as an additional increment to the discount rate — the CRP reflects verified country-level data only, which keeps the WACC auditable.

4.1.2 Cost of Debt

| Component | Value |

|---|---|

| Pre-tax Cost of Debt (Kd) | 6.41% |

| Marginal Tax Rate | 38.25% |

| After-tax Cost of Debt | 3.96% |

The pre-tax cost of debt is derived from actuals: FY2025 interest expense divided by average total debt across FY2024–FY2025, both taken from the verified workbook. This actuals-based approach was chosen deliberately over a coupon build-up because the debt footnote in the FY2025 filing states the coupon on the newest notes inconsistently in two places — a forensic watch item — and deriving Kd from cash interest paid sidesteps that ambiguity entirely. The resulting 6.41% is consistent with the company’s credit profile: an all-fixed-rate, US-dollar bond stack with long-dated maturities and no maturity wall, where the blended rate reflects legacy low-coupon issuance alongside the more expensive 2025 vintage. The after-tax cost applies the projected marginal tax rate of 38.25%, which is the trailing three-year average effective rate stepped up for the enacted increase in the Mexican special mining duty effective 2025 — the same rate used throughout the DCF (see 4.2.1).

4.1.3 Capital Structure & WACC

| Component | Value |

|---|---|

| Equity Weight (market value) | 98.3% |

| Debt Weight (market value) | 1.7% |

| WACC | 11.48% |

Source: approved valuation assumptions (valuation_assumptions.json) and market_data.json; capital-structure weights at market values using net debt — market capitalization 142,890.5M against net debt of 2,446.1M (total debt 6,750.7M less cash 4,304.6M).

At 98.3% equity and 1.7% debt at market values, the capital structure is near-zero leverage for discounting purposes — a consequence of the market capitalization dwarfing a modest net debt position. The practical implication is that the WACC of 11.48% is, to within rounding, the cost of equity: the cheap after-tax debt is too small a sliver to pull the blended rate down meaningfully, and the WACC moves essentially one-for-one with any change in Ke while being almost completely insensitive to the cost of debt. The discount rate debate for this name is therefore entirely an equity-side debate — beta, the equity premium, and above all the country risk premium — and the sensitivity analysis in 4.3 should be read with that in mind. Market-value weights are used throughout; the company discloses no management leverage target, and the book-value capital mix is irrelevant for this purpose.

4.2 DCF Model — Three Scenarios

sources The DCF uses a five-year explicit projection period plus a terminal value. Five years is the right window for this asset: reserve life is multi-decade, but the only dated, fully committed catalyst is the Tía María project with its targeted 2027 start-up; beyond the ramp of that project the business is steady-state and the terminal value captures it, so a longer explicit window would add assumption risk without adding information. Terminal value is computed under two methods — perpetuity growth and exit multiple — with the selected method and the rationale for the choice shown in 4.2.3. Three scenarios are run: Base, Bear and Bull, differing in revenue growth, EBITDA margin and terminal growth per the standard adjustments below. All three scenarios discount at the same WACC — the scenarios test operating outcomes, not the discount rate, which is stress-tested separately in 4.3.

4.2.1 Key Assumptions

sources | Assumption | Bear | Base | Bull | |—|—|—|—| | Revenue Growth — each year | Base − 2pp | 6.0% (Y1) → 3.0% (Y5) | Base + 2pp | | EBITDA Margin — each year | Base − 1pp | 55.0% (Y1) → 56.0% (Y5) | Base + 1pp | | CapEx / Revenue | unchanged | 12.0% (Y1–Y2) → 10.0% (Y4–Y5) | unchanged | | D&A / Revenue | unchanged | 6.5% (Y1–Y2) → 7.0% (Y3–Y5) | unchanged | | Δ NWC / Incremental Revenue | unchanged | 15.0% | unchanged | | Effective Tax Rate | unchanged | 38.2% | unchanged | | Terminal Growth Rate | Base − 0.5pp | 2.5% | Base + 0.5pp | | Exit EV/EBITDA Multiple | 9.0x | 9.0x | 9.0x | | WACC | 11.48% | 11.48% | 11.48% |

Note: Bear and Bull use the standard adjustments above (per the valuation-agent methodology), applied to every projection year. The resulting fair values appear in Section 6.2 ($44.83 / $59.86).

Revenue growth path. Year-1 growth of 6.0% sits well below the trailing three-year revenue CAGR documented in Section 3 and dramatically below sell-side consensus for FY2026 — a deliberate and, relative to the street, aggressive act of conservatism that should be understood as such. The reasoning: FY2025 revenue was set at record copper prices and, as Section 3 details, included a positive mark-to-market on provisionally priced, unsettled copper sales that is exposed to reversal in early FY2026 if prices retrace — and copper has in fact retraced from its highs. Consensus revenue estimates predate that retracement. The base case therefore assumes price normalization rather than extrapolation. Year 2 steps up to 7.0% as Tía María — the committed greenfield project targeted for 2027 start-up, adding cathode capacity equivalent to a meaningful slice of current copper volume — begins to contribute, with Year 3 at 6.0% capturing the full ramp on flat prices. Years 4 and 5 fade to 4.0% and 3.0%, converging toward the terminal rate, because there is nothing dated behind Tía María: the next projects in the pipeline are either physically obstructed (Los Chancas) or a decade-plus away (Michiquillay), as Section 2 develops. Growth in this model is volume-led, not price-led — the opposite of what drove the FY2025 print.